Earnings Day: AMZN, GOOG, MSFT

The Night the AI Capex Thesis Stopped Being a Question

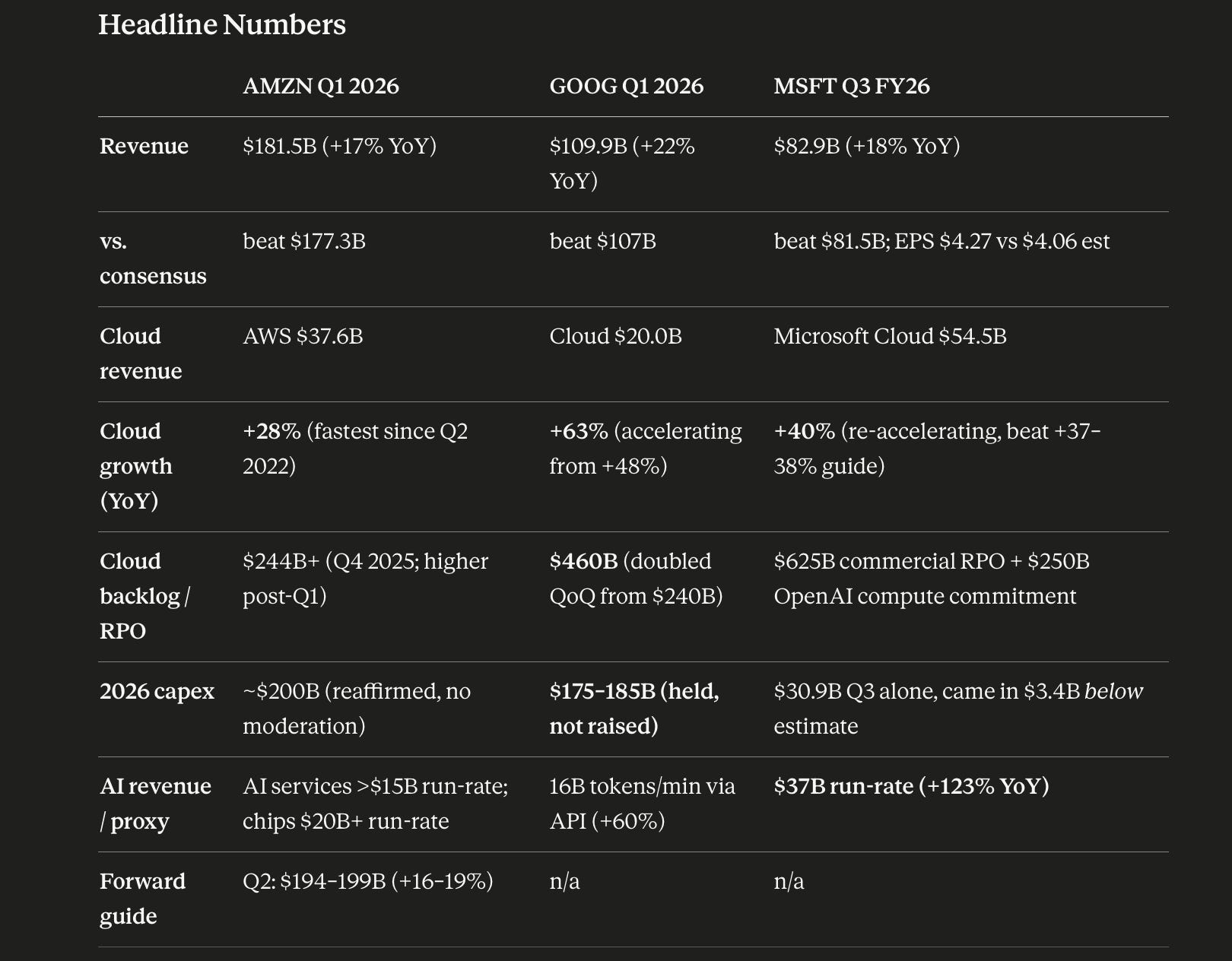

What a day of earnings we just had. Three mega caps put out numbers in a single ten-minute window. Combined: $480B of revenue, $120B of cloud revenue growing anywhere from 28% to 63% depending on the name, and a $1.5T contract backlog.

The trillion dollar question is whether AI infrastructure is actually earning its cost of capital. Tonight, three different names gave three different answers.

What Was Reported

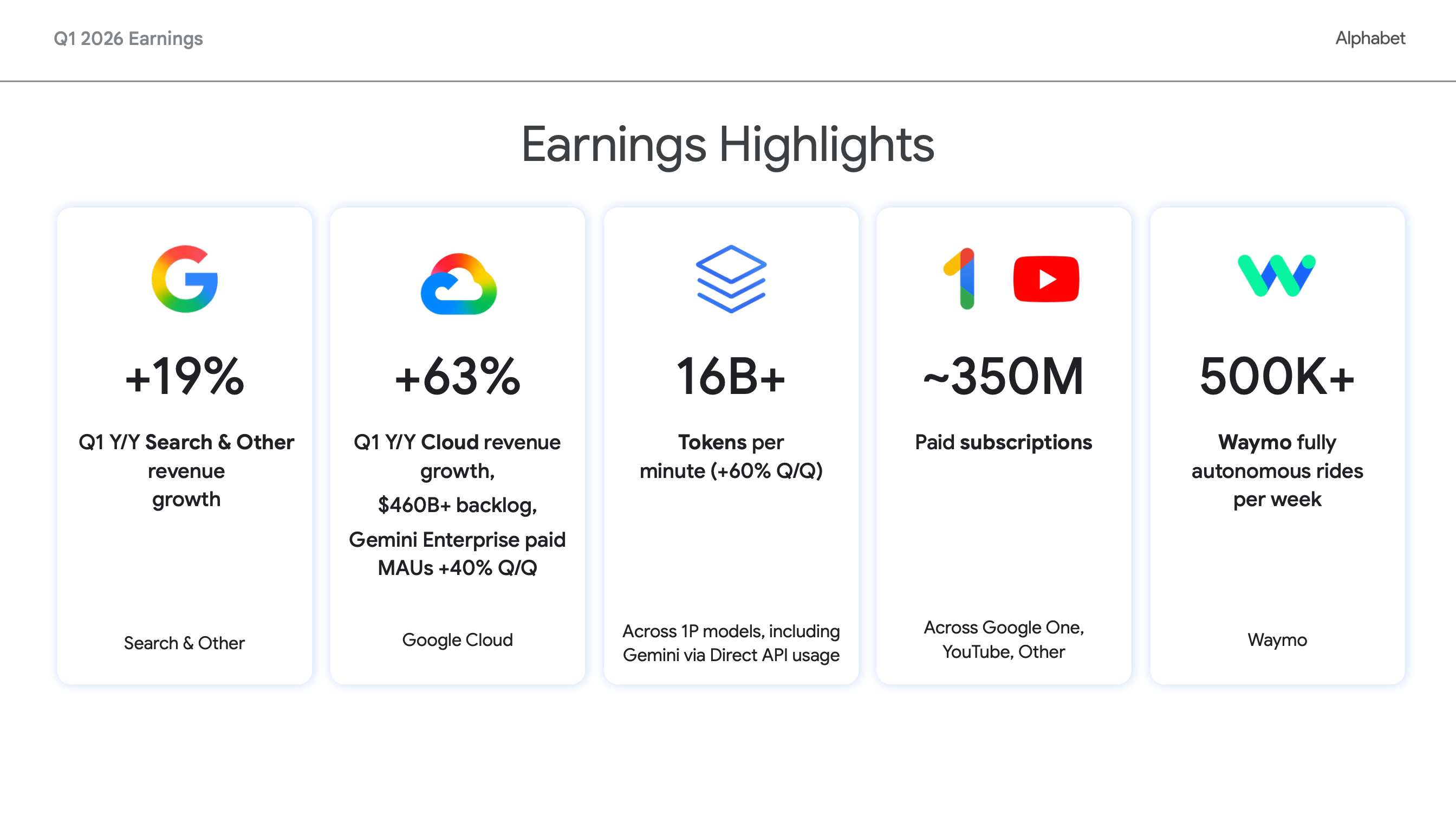

Alphabet gets the prize for best slide. Search is clearly not dead at 19% YoY, Cloud is killing it at 63% growth and a $460B backlog, 350M paid subscriptions, and Waymo (the side project that isn’t a side project anymore) is hitting 500K autonomous rides per week. I still haven’t tried it.

The table here tells the rest of the story for the three behemoths:

Amazon

Highlights for Amazon include operating income of $23.9B versus the $21.5B guide. AWS grew 28%, its fastest rate since Q2 2022.

Alphabet

Cloud up that whopping 63% we already mentioned, accelerating from 48% the prior quarter. It’s worth saying clearly that these are huge numbers. $20B for Google Cloud is the segment, and putting up double-digit growth at that scale would have been unthinkable a decade ago.

The backlog has also doubled and operating margin grew 200bps to 36.1%. All around a fantastic quarter and the cleanest possible answer to “does the spend earn its cost of capital.”

Microsoft

Total revenues were $82.9B (+18%). AI-related revenue grew 123% YoY to a $37B run rate. There’s also a solid $625B backlog.

Now the kicker: Q3 capex came in at $30.9B. That’s $3.4B below estimate. Microsoft was the only mega cap to announce spending less than expected, and that’s worth digging into.

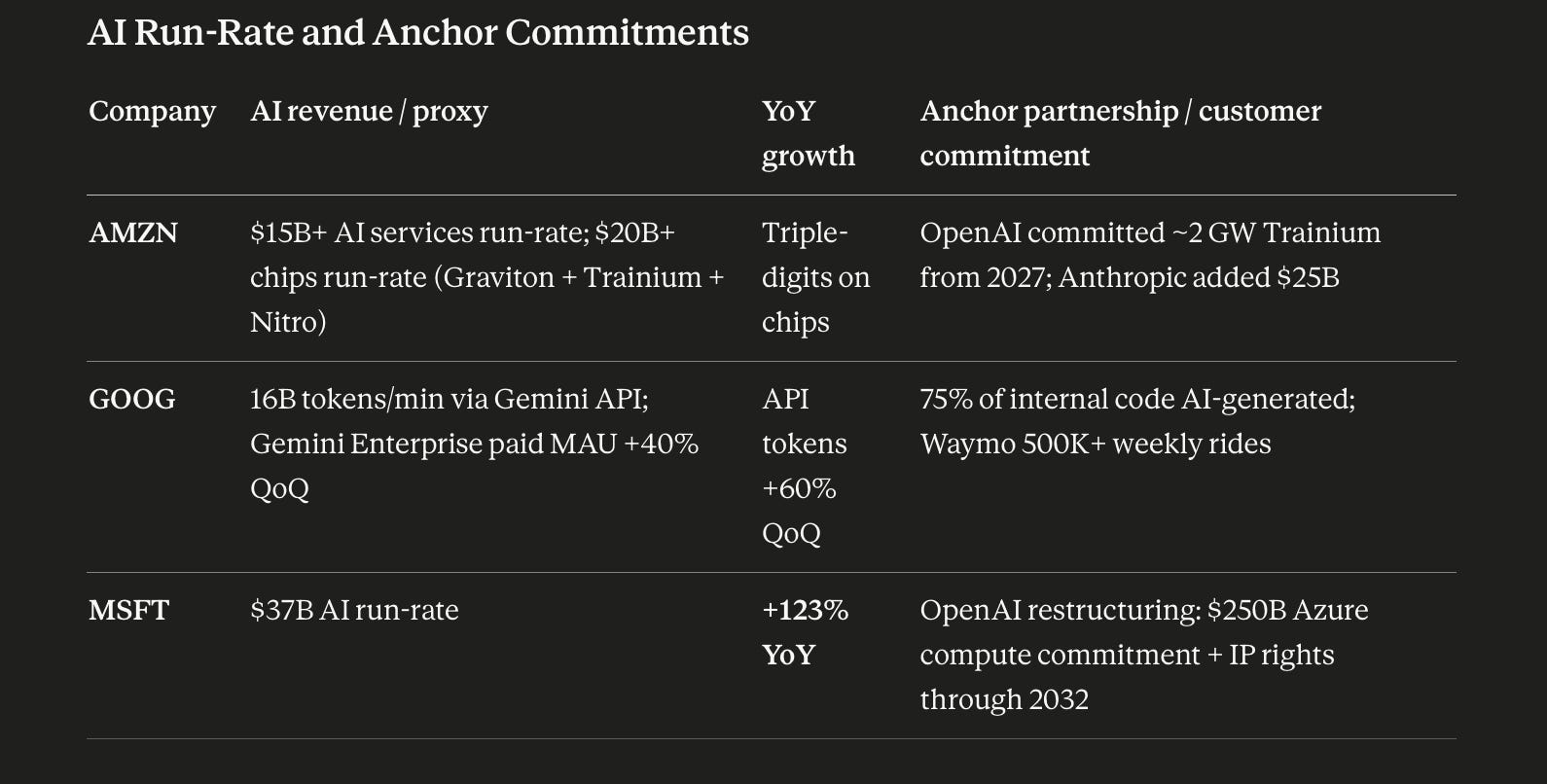

Here’s a look at the AI-related items I was able to extract from the earnings releases.

Microsoft’s Capex Tell

We just mentioned it, but buried in Microsoft’s Q3 release was the most underrated number of the night. I haven’t really seen anyone discussing it.

Capex came in at $30.9B, $3.4B below Wall Street estimates.

Compare that to the rest of the field:

Amazon reaffirmed $200B in spending for 2026. No moderation, no scaling back, no scaling up.

Google held the $175B to $185B commitment. They didn’t raise it, didn’t cut it.

Meta raised spending by $10B to $125B–$145B and suspended buybacks.

Microsoft spent $3.4B less than expected and still re-accelerated Azure to 40%, while printing 123% YoY growth in AI revenue.

The demand side of the AI capex thesis is no longer a question. Three of the four companies confirmed the spending is monetizing as expected. The return side, whether this earns its cost of capital across the cycle, still needs another four to six quarters of margin data to settle.

What’s already settled is the differentiator. Going forward, it isn’t who spends the most. It’s who spends the most efficiently. Tonight, only one of these companies actually put up a strong quarter while spending less.

This is a post-earnings write-up, but I want to explore this idea in a future article. If you haven’t signed up for Tech Breakdowns yet, please do so and we’ll get back to it in a week or two.

TechBreakdown’s Octagon

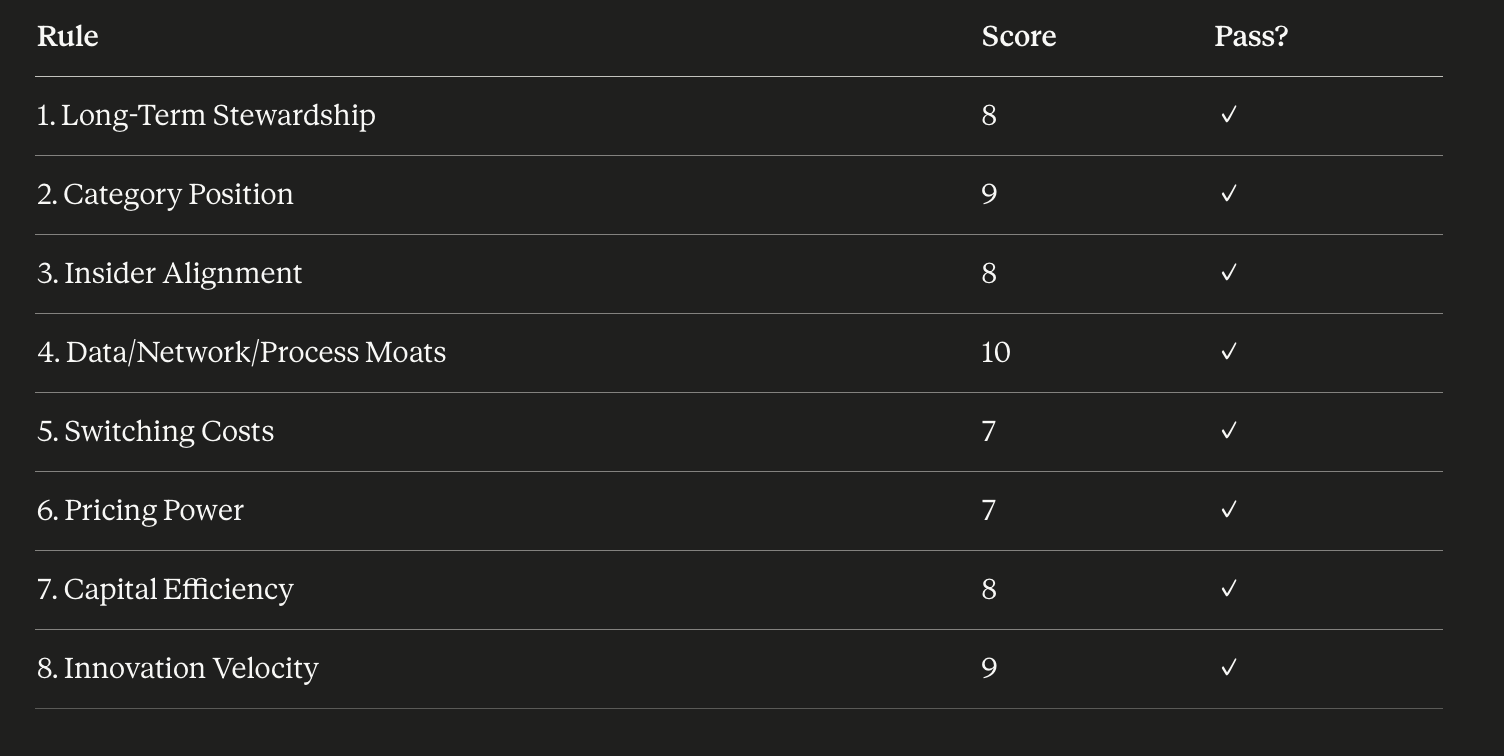

This is a new publication, so we haven’t fully introduced the Tech Breakdowns Octagon yet. I promise a full write-up of the rationale soon. For now, just know that the Octagon is the eight-rule scoring framework I use on every Tech Breakdowns Format A piece.

Today, I want to touch on the three names in this article. All three score an 8 out of 8.

It wasn’t like that before earnings. Amazon was sitting at a 7 going in, with a slight reduction on Rule 7 (capital efficiency). Today that flipped from a 5 out of 10 on capital efficiency to a 6 out of 10. The capex thesis they’ve been running, all this spending, went from promise to actual proof. I’m still scoring it a 6 because of the extended capex spend, but it’s at least trending in the right direction.

The eight rules, briefly:

Long-term stewardship.

Category position. Specifically, is it a category leader in its segment.

Insider alignment.

Data, network, or process moats.

Switching costs. How likely or easy is it to switch away from this provider.

Pricing power. Can they raise prices without losing customers.

Capital efficiency. For these three companies in particular, what does capex look like. There’s some M&A read-through here too.

Innovation velocity.

This is a qualitative score, but I run it on every company we cover. It tells me whether this is a business I want to own and hold for the long term. You’ll notice price isn’t in here. That comes later. Each company gets a 1 to 10 score on each rule, passes a rule at 6+, and the aggregate is the count of rules passed out of 8.

For Google, Microsoft, and Amazon, the final score is a perfect 8 out of 8 as of earnings.

Here are the actual scores I give for each company.

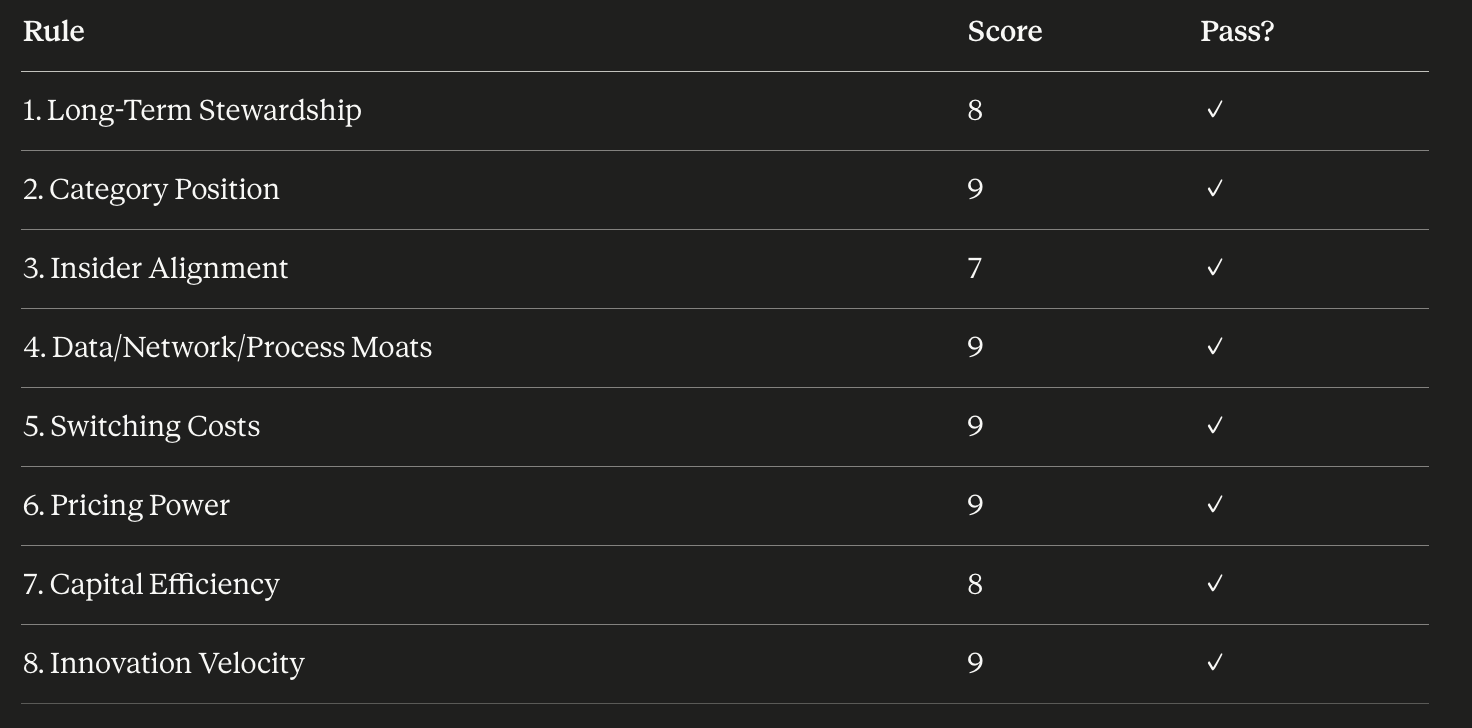

Alphabet

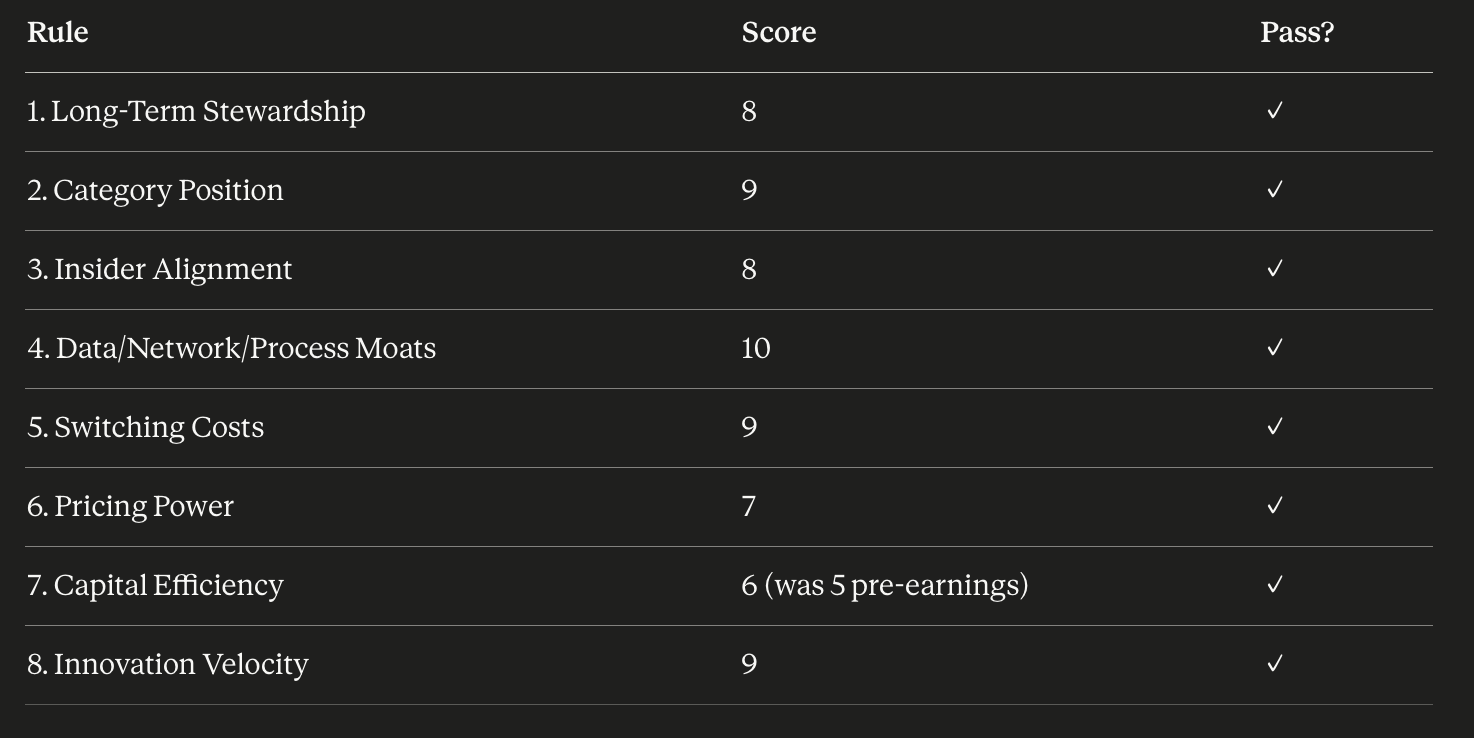

Microsoft

One thing worth flagging on the Microsoft scorecard: it grades higher than Alphabet on both pricing power and switching costs. That isn’t a vote against Google, it’s a feature of how deep Microsoft is embedded in the enterprise stack. Active Directory, Office, Teams, GitHub, the ISV ecosystem on Azure. Multi-decade integration with sticky pricing on top. The framework is telling you something the valuation section will confirm.

Amazon

Valuation Outlook

The scores are great. They show these are high-quality businesses, which I don’t think anyone really disputed. The next question is whether right now is a good time to be buying.

I look at three things.

First, expected long-term annual return. FCF yield plus long-term growth.

Second, margin of safety on the implied growth, built using a reverse DCF.

Third, a multiple sanity check. Forward P/E or EV/forward FCF versus the historical 5-year range. For some companies I’ll adjust for cycle position and capex normalization.

Google. FCF yield is roughly 2.5%. Implied growth in the reverse DCF is sitting in the 9% to 10% range, which Alphabet has historically beaten, but the margin of safety is thin. Forward P/E is around 22 to 24x, which is closer to the upper half of the 5-year range than the lower. Middling on rule one, middling on rule two, middling on rule three. This one falls into the hold bucket.

Microsoft. FCF yield of 3.5%, which is a much nicer place to start. Decent margin of safety on the reverse DCF. Forward P/E is sitting at 22 to 24x, which is well below the 5-year average of 30x. The multiple has actually contracted through one of the strongest fundamental stretches in the company’s history.

Amazon. FCF yield of 3%, which is fairly decent for a company in Amazon’s position. Implied growth is 11% to 12%. Forward P/E is 31 to 33, sitting at the 5-year low. The multiple appears to have compressed precisely because the market is mispricing the temporary capex-driven free cash flow dip.

For the long-term holder

I’m a long-term stockholder, which means I’m looking for excellent companies at fair prices. The Warren Buffett line, a wonderful company at a fair price, is what I’m after. I lead with discipline, but I also don’t cut names like Google just because they’re slightly overvalued at a point in time. Google still has a lot of potential. I also don’t want to incur a tax bill by selling it in my taxable portfolio.

NVIDIA is a useful reference point here. NVIDIA in early 2023 was an 8 out of 8 shaped business, and it 5x’d in the following 18 months. The same NVIDIA in 2021 was also an 8 out of 8, and it lost 60% in the next 12 months. Same quality, different prices.

On that spectrum, Amazon and Microsoft today look closer to the 2023 setup. Google looks closer to the 2021 setup. That doesn’t mean Google goes down 60%. It means the entry price is doing more of the work.

A framework’s job is to keep us honest. If everything that beat earnings was a buy, you wouldn’t need a framework. Google isn’t a “don’t own.” It’s a “don’t add.”

Of the three, Google is still the one I most want to buy from a future-position point of view. Search grew 19% YoY. I have no idea how Google Search keeps growing at 19% on this base. It has to be one of the greatest businesses ever built, and Google keeps bolting new businesses onto the side of this rocket ship. I don’t know where that company ends. I’m holding for the long term.

I took a small nibble on Amazon when it dipped post-earnings. It was only a tiny one because it’s been a name I held for years. I sold earlier this year when I got bored of waiting for the company to actually do something. Of course it did something after I sold. I’m back in now for a little bit, mainly to keep tabs on it and to have it in the portfolio.

Microsoft is more of a personal take. The numbers are stellar and the business is firing on all cylinders. My bias: I prefer GCP and AWS as products, and I’m not sold on Copilot Chat as the consumer-facing front end. That’s a taste claim, not a thesis, and the numbers don’t care about my preferences. I’m flagging the bias rather than dressing it up.

Closing

It was a fantastic night of earnings for three of the largest companies on Earth. All three knocked it out of the park. All three remain stellar businesses.

The most intriguing from a “should I buy right now” point of view is Amazon. Google is the one that keeps catching my eye even at a stretched valuation. I’ll continue to hold it as a core position.

More on the capital efficiency angle in a future piece.