The Invisible Bottleneck in the AI Data Center: AOI Breakdown

How microscopic lasers, grown from the crystal up, are replacing copper wire to keep hyperscale networks alive.

In today’s breakdown we’re going to take a look at a company that is pretty close to me, at least geographically. The founders of this company were part of the University of Houston, which is my alma mater. They also came from and worked at NASA’s Johnson Space Center, a place that I live just a few minutes away from.

The company is Applied Optoelectronics, or AOI. That company is largely based a little bit down the road from NASA’s Johnson Space Center today, in Sugar Land, Texas.

This is a company that has run from $15 a share to $200 plus per share in the last year. These things take me a few days to put together and publish, so there’s a good chance that by the time you’re reading it, it’s nowhere near $200 a share. Could be back down at $15, could be up at 600. We just don’t know.

But part of this publication is not always finding the perfect companies to buy. It’s digging in and understanding what these companies are, what they do, and then ultimately making a decision as to whether now is the right time, or whether maybe there’s just not enough juice left in the squeeze. That’s a perfectly fine outcome too.

So ultimately, we’re looking to answer whether there is a valid business under all this, or whether it’s all smoke and mirrors that will eventually lead to ruin for those that are getting in at this $200-per-share mark.

What is AOI?

AOI is a vertically integrated optical maker. If that means nothing to you, don’t worry, because hopefully by the end of this section it will.

Now all around us we have cables, and those cables are sending data back and forth. As I write this I am watching the Stanley Cup Finals on a TV that has an HDMI cable. That HDMI cable sends a signal back and forth. It has Ethernet plugged into the back of it, and that Ethernet is sending a data signal back and forth.

Now most cables that we interact with, most cables that we’ve dealt with over our lives, have been made of copper. Copper is great. Copper can send these signals for decently long distances and it has a lot of strengths. Ultimately, when it comes down to it, copper just can’t handle fast signals, and the world that we are rapidly heading towards requires fast signals.

If you look at the data center buildouts that are happening, these data centers all have racks and racks of GPUs. To be able to build the types of models that we are seeing from these AI powerhouses, you need to be able to connect GPUs, and you need those connections to be fast. That’s where optical makers come in. They are not building these connections out of copper wires any more. They are building these connections out of lasers and light.

And that’s where AOI sits. It helps make these transceivers and the technologies that are required to send a signal back and forth between different racks in these data centers. Sounds simple, but there’s actually a lot of tech that goes into it.

Right now the product that is really driving the price in AOI up is called an EML transceiver. This particular piece of technology helps send a signal back and forth between different racks, or between wherever you need that signal to go. Right now 800G is the big buildout. All the data centers want 800G. This is a 100Gb connection across eight different lanes, which means you can send a ton of information back and forth. A lane is just one of those parallel streams of light. Stack eight of them at 100 gigabits each and you land at your 800 gigabits.

There’s a lot of fun physics that I got into as part of researching for this article, which I won’t bore you with. I was actually pleasantly surprised by a primer on the physics that Claude provided me. So, yes, I definitely used some transceivers in the making of this article.

Alright, where were we. AOI. Well, the thing I want to call out here is that this is not AOI’s first rodeo when it comes to catching onto a massive buildout trend, and it’s actually one of the most alarming things I found about this company. AOI is a pretty old company. It’s been around for a good long while. It’s been in the cable business. It’s been in all kinds of businesses. It’s been around that long.

In 2017 the stock had explosive growth on the back of Amazon. So Amazon shows up, they’re building AWS, and AOI was the company that was helping them build the transceivers for it. Instead of 800G this was 40G and 100G at the time. This sent AOI stock up to $100 a share into 2017, and it ultimately ended up busting down to $1.48 when it turned out that Amazon didn’t need anywhere near the volume everyone had built up for.

I mention this not as a guarantee of the path that we’re on, but just to highlight that we have been on this exact path before. The parallels are eerily similar. In 2017 Amazon was by far the largest customer, and the ten largest customers AOI had made up greater than 95% of the company’s revenue. In 2026 the concentration is just as extreme. The top ten customers again make up more than 95% of revenue, and just two of them, a cable distributor named Digicomm and Microsoft, are better than 80% of the total. Different names, same shape. Not a guarantee of things to come, but a path to be wary of.

And this kind of thing happens because of cyclicality. We will touch on cyclicality later in the article.

The Technology Transition

800G, as we have mentioned, is EML. There are a few different types of products that exist in this space, but 800G is dominated by EML, and EML happens to be exactly what AOI is built around.

What is going to happen as we move forward is a significant shift in how the market works. This shift happens at 1.6T, and especially at 3.2T, where silicon photonics takes share and the value migrates from this high-margin EML to cheaper CW lasers.

The next question you probably have is whether AOI is participating in 1.6T. Yes, AOI is a real 1.6T participant. But what we need to be aware of is that it will not be a dominant participant in CW lasers, where there are already significant competitors. It’s also a world with lower margins, and a world that is more contested.

The good news, though, is that one of AOI’s significant advantages still plays out in the CW laser space. Their vertical integration. In late 2025 they announced their own high-power CW pump laser aimed right at silicon photonics and co-packaged optics, which is their way of trying to keep a foot in the next generation rather than just defending the last one.

We touched on vertical integration above but did not go into it in depth. A thing worth knowing about AOI is that it is incredibly vertically integrated. It goes all the way from growing the crystals that are required in the end product, all the way to delivering the end product. Competitors have to rely on others for different parts of this. AOI simply does it all itself.

And AOI is building the newest of this capacity, the 800G and 1.6T lines, inside the United States, down in Texas. Right there are two things that work in AOI’s favor versus its competitors.

AOI is not the market leader in high-end EML lasers. That title belongs to Lumentum. It is not the leader in 800G module volume. That title belongs to InnoLight. But AOI’s real edge is that it makes its own lasers and its own modules, in the United States, from the ground up. It’s not waiting in Nvidia’s allocation line, and it’s geopolitically very clean.

Competitors

There are a number of competitors in the space. You have the aforementioned Lumentum. Lumentum is the EML laser leader. This is the 800-pound gorilla in the room when it comes to EML lasers. They own about 60% of the market and they’ve been rewarded heavily for it. This is roughly a $70 billion company at the time of writing, and it has run more than tenfold over the past year. It was one of the best-performing stocks in the entire S&P 500 this year, and it just joined the Nasdaq-100.

Coherent is another competitor. Coherent broadly builds EML plus SiPh. SiPh is cool, or silicon photonics. This is the technology of building the optical circuits directly onto standard silicon microchips.

InnoLight and Eoptolink are the volume module leaders out of China, and they compete on a pure cost basis. These are the companies that pump stuff out cheap. Sometimes cheap is good, but this is also a supply chain risk, which is part of why AOI stands to benefit from being stateside.

I called Lumentum the gorilla in the room, but the true gorillas are companies like Broadcom. Broadcom makes the DSP chips and the switch silicon that sit at the very center of these networks, which is a different layer from the lasers and modules AOI builds. DSP stands for Digital Signal Processing, and it is the chip inside a transceiver that cleans up the signal so it survives the trip. Broadcom builds those for 800G and 1.6T, and it is also out front on CPO.

And CPO is another term you’ll want to be familiar with if you are interested in investing in semiconductors. CPO stands for co-packaged optics. Traditionally a switch chip uses electrical traces to send data to pluggable lasers on the front edge of the server rack. CPO integrates the optical silicon directly next to the switch ASIC on the same package. So it eliminates the copper travel distance, slashes power consumption, and reduces latency for these massive hyperscale networks.

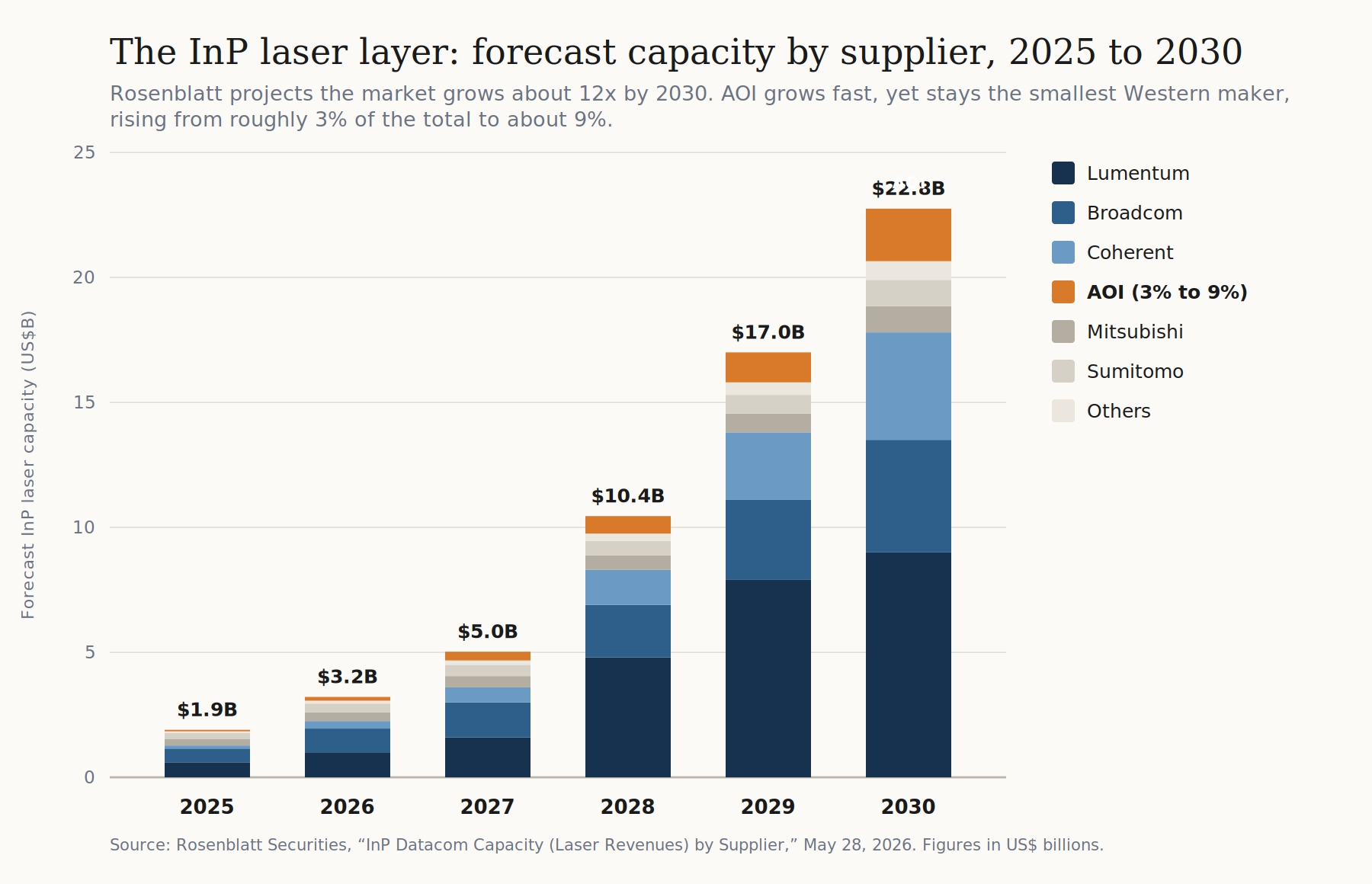

Amongst all these names, AOI is the small, vertically integrated Western player. Of all the Western InP laser makers it is the smallest, which generally means it’s got more room to grow.

The Financials

Let me walk you through the numbers, because this is where the story gets real on both sides.

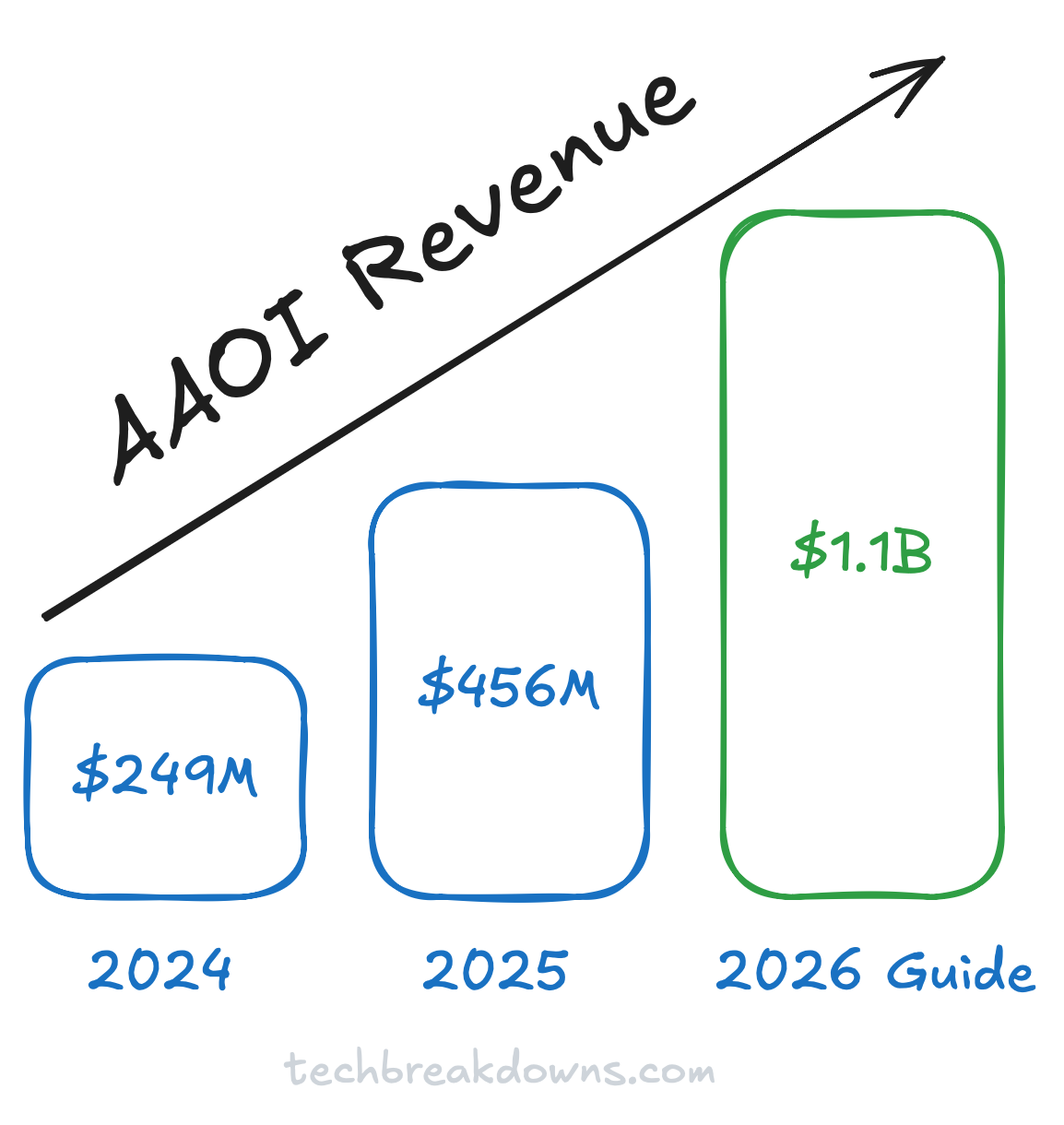

Start with the top line, because the top line is the whole reason anybody is paying attention. In 2024 AOI did about $249 million in revenue. In 2025 it did about $456 million. That’s an 83% jump. For 2026 management is guiding to more than $1.1 billion, which would be better than doubling again. So you’ve got a company going from a quarter of a billion to over a billion in revenue in two years. That is the kind of slope that takes a stock from $15 to $200.

The most recent quarter, Q1 2026, reported on May 7, was the fourth record quarter in a row. Revenue was $151 million, up 51% from a year earlier. Data center was $81 million of that, more than half the company now and up over 150% year over year. Cable chipped in $67 million. So the AI data center business has officially become the main event.

AOI still loses money, and I am not going to dress that up. Q1 was a GAAP net loss of $14 million. Gross margin was about 29%, which actually slipped a little from the quarter before as the data center mix grew. One detail the headlines skipped right over: of that $81 million in data center revenue, only $4.6 million was actually 800G. The big 800G ramp hasn’t really happened yet. What grew in Q1 was the older 100G and 400G product. The 800G wave, the one this whole thesis rides on, is a second-half-of-2026 event.

This matters, because AOI has never put together a sustainably profitable year in its entire life as a public company, going all the way back to its 2013 IPO. Full year 2025 was a loss of about 26 cents a share.

So why does anyone care? Because management says that changes this year. They are guiding 2026 to more than $140 million in non-GAAP operating profit, and they expect to flip to non-GAAP profitability starting in the second quarter. They’ve laid out 60% to 80% sequential revenue growth in the back half as new Texas capacity comes online, with gross margins climbing to 35% by year-end and over 40% in 2027. A company that crosses from years of losses into real profit while doubling revenue can re-rate hard. That’s the bet.

And the number management keeps pointing at sits even further out. On the call the CFO put a hard figure on mid-2027: roughly $471 million a month in data center transceiver revenue. Annualize that and you get about $5.65 billion in transceivers alone, before a dollar of cable. The current full-year guide is $1.1 billion. So management is telling you the exit speed eighteen months out is something like five times this year’s number. The CEO literally called this year’s $200 million-plus orders small compared to what is coming.

Last, the balance sheet, because building laser factories is not cheap. AOI exited Q1 with about $449 million in cash, but a big chunk of that came from a $382 million stock raise during the quarter. There’s also $125 million of convertible debt due in 2030. The company is spending heavily on capex, burning cash, and funding the buildout by issuing stock. That keeps the lights on and the factories going up, but it means the share count keeps creeping higher, and every new share is a slice of the pie taken out of the existing owners’ hands. Hold that thought for the bear case.

Cyclical or Structural

I promised we’d come back to cyclicality, so here we are. Everything in the bull and bear cases below hangs on it.

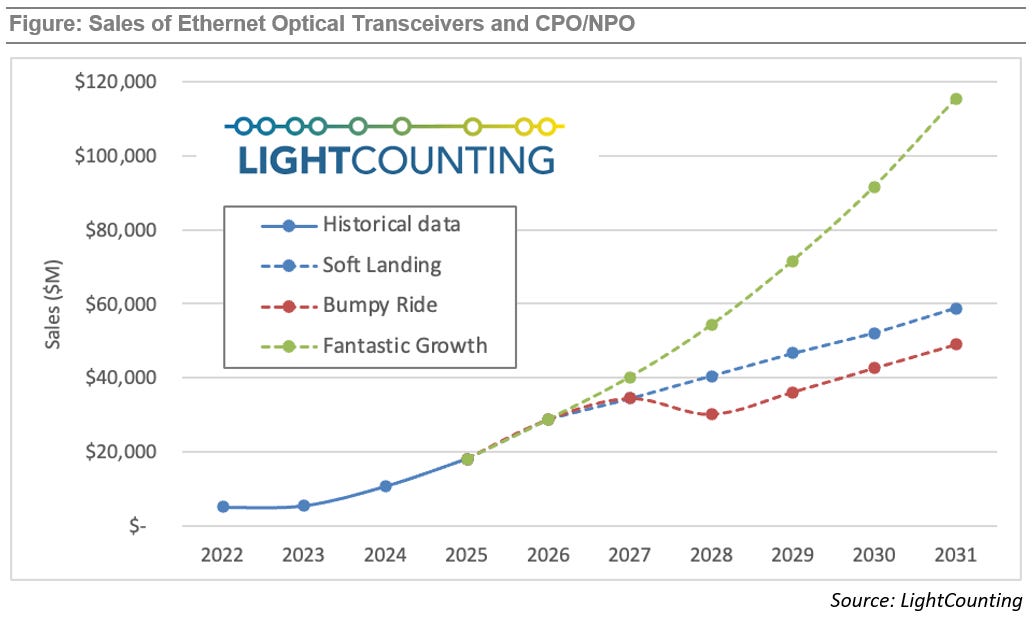

The optical business has always been cyclical. Wildly so. If you’ve ever looked at memory chips, at companies like Micron or SK Hynix, you know the pattern. Demand grows for a couple of years, everybody races to add capacity, capacity overshoots, prices crash, and the whole industry has a miserable year before it does it all again. Optical transceivers have run on that same rhythm for two decades. The firm LightCounting, which tracks this market more closely than anyone, has pointed out that every two or three good years gets interrupted by a flat or negative one. And the down ones are not gentle. The last big cycle, the 2017 to 2018 one that AOI rode and then got crushed by, saw these stocks fall 50% to 70%.

So how does that happen, mechanically? It usually isn’t pure overbuilding by itself. It’s the inventory whipsaw on top of it. When parts are scarce, customers panic and over-order from every supplier they can find, building a stockpile just to guarantee they get their allocation. The moment the shortage eases, they cancel the duplicate orders and start working down that stockpile. Reported demand falls off a cliff even though the real end demand is fine. Then, because everyone added capacity during the boom, there’s now too much of it, and suppliers start competing on price. That’s the cycle. And the dangerous part is that it tips right at the moment the shortage ends.

LightCounting expects the current laser shortage to ease around the middle of 2026. They are explicitly calling for a flat quarter or two in late 2026 as the supply chain finds its footing. That is the next test.

Now the other side. This time might genuinely be different, at least in degree. In every past cycle, one speed generation ramped, peaked, and got replaced by the next, in sequence. This time the generations are stacking on top of each other. 800G is ramping, 1.6T is ramping right behind it, 3.2T is coming, and co-packaged optics adds a fourth layer behind that. Because demand is spread across so much of the stack at once, no single generation’s inventory hangover can sink the whole thing the way the 100G glut did in 2018. That is the single best argument that the next downturn could be shallower than the last.

The demand itself has a self-feeding quality this cycle. Every new AI model generation increases the amount of inference running, which means more hardware, which means more optics, on a loop. And the network is eating a bigger and bigger share of every data center dollar as clusters get larger. So the trend line is real, and it is steeper and more durable than memory’s ever was.

But, and this is the honest synthesis, structural growth and cyclicality are not opposites. Memory demand has compounded for forty years and memory is still the most violently cyclical business in tech. Both things are true at once. The market growing to $35 billion or more by 2030 and the industry having brutal down years on the way there are not in conflict.

The cleanest tell that even the biggest players expect the cycle to persist is this. Nvidia reportedly asked the laser supply chain to build 20 times more capacity by 2030, and the suppliers pushed back and agreed to only 12 times (per Rosenblatt Securities’ May 2026 indium phosphide supply model). People who believed in permanent, non-cyclical demand do not deliberately under-build. They are hedging against the down year they know is coming.

So where do I land? This is structural growth wrapped around a cycle. The decade trend is up and to the right, steeper than memory. But there will be air pockets, the demand sits in the hands of a few spending-cyclical buyers, and the first real test arrives in the back half of 2026. For a company like AOI, which we’re about to see is concentrated, richly valued, and not yet profitable, the cyclicality is not a footnote. It’s the main risk.

Bull Case

Alright, let me lay out the bull case as strongly and as honestly as I can, because there is a real one here.

It starts with a moat that’s easy to miss. Everybody in this industry can design an 800G transceiver. The incumbents can all do it. The hard part is not designing one. The hard part is building enough of them, precisely, at a cost that scales. Inside every transceiver is a microscopic assembly of lasers and waveguides where a misalignment of a fraction of a hair kills the signal. And remember what we covered in the technology section: silicon cannot make light, so every one of these things needs an indium phosphide laser, and those lasers are the single most supply-constrained part of the whole industry. There aren’t enough of them, and the furnaces that grow them are booked solid.

AOI is different because it makes its own lasers. In-house. The exact part everyone else is fighting to source, AOI grows itself, from the crystal up. And it goes further than that. It builds its own automated production lines, and, more importantly, much of its own manufacturing equipment. So when the CFO got the obvious bear question on the call, which is, fine, demand is huge, but can you actually build it, his answer was that equipment availability hasn’t been a problem because they make most of the equipment themselves. While competitors line up for the same furnaces, the same merchant lasers, and the same third-party tools, AOI is not standing in any of those queues. The moat here is not a patent. It’s throughput nobody can copy on a short timeline.

Then there’s the order book, and these are signed orders, not a slide deck. In March, AOI announced its first volume 1.6T order from a major hyperscaler, worth more than $200 million, big enough on its own to put that one customer back above 10% of revenue. It booked a $53 million 800G order, then another $71 million one. That’s over $324 million from a single hyperscaler in about four weeks. And when an analyst asked why that $200 million 1.6T order stretches into 2027, the CEO’s answer was that it’s small compared to what’s coming in 2027.

Stack the capacity ramp behind it. AOI exited Q1 making about 100,000 of these units a month. The plan is 150,000 this quarter, over 650,000 a month by the end of 2026, and over 930,000 a month by the end of 2027, with more than half of that built on US soil. Management calls it the largest US production capacity for 800G and 1.6T.

Put it together and the bull case is this: a company that owns the scarce input, can build at a speed nobody else can match, is sitting on signed hyperscaler orders, and is about to cross from years of losses into real profit while its revenue multiplies. Add a genuine strategic edge in US manufacturing, which the hyperscalers increasingly want for supply security and tariff reasons, plus an Amazon that has tied its own stock warrant to how much product it buys.

But I want to state the bull case fully, including its shape, because the shape is the risk. The bull case, completely stated, is a pre-paid, high-beta execution bet on a 9x capacity ramp landing on schedule, into a demand environment that has to stay vertical. Every word in that sentence is doing work. Pre-paid, because you are paying for it now, today, before it happens. Execution bet, because the capacity actually has to get built. And demand that has to stay vertical, because if the AI spending cools, all of it cools with it.

Bear Case

Now the other side. A thesis you can’t argue against is not conviction, it’s hope. So here’s the honest bear case.

Start with the price, because the price is the problem. At around $200 the stock trades at roughly 15 times this year’s sales, for a company that has never strung together a profitable year. A lot of very good news is already baked in. As we’ll see in the valuation, even a genuinely good outcome is largely priced in today. That leaves very little room for error, and this is a stock that does not handle error gracefully.

Then the concentration, which is the biggest risk by a mile, and the one that should make the hair on your neck stand up given the history. The top ten customers are about 97% of revenue. Two of them are more than 80%. And AOI sells on purchase orders, not binding long-term contracts, so there’s no floor under any of it. The famous $4 billion Amazon figure is a discretionary ceiling, not a commitment. We’ve watched this exact movie before. In 2017 one giant customer was most of the revenue, the orders dried up, and the stock went from $100 to $1.48. Nobody is saying that happens again. But the structure that made it possible is sitting right there on the page, unchanged.

Next, the technology, which is the slow risk rather than the sudden one. AOI’s strength is the EML, and the EML is exactly right for 800G. But the industry is moving toward silicon photonics and cheaper CW lasers at 1.6T and beyond, and in that world the value drains out of the expensive part AOI is best at. AOI is in that race, but by Rosenblatt’s own numbers it is the smallest of the Western laser makers, well behind Lumentum and Coherent. So the bull case is partly leaning on a technology whose long-term share is genuinely in question.

Add that the profitability is still a promise. The 35% margins and the $140 million of operating profit are forecasts, not results. And the most recent quarter actually missed on revenue versus what Wall Street wanted, while the next quarter’s guidance came in a touch light. This is an execution bet, and the execution hasn’t been flawless.

Then the dilution we flagged earlier. The buildout is being funded by selling stock, and the convertible notes and the Amazon warrant are more shares waiting in the wings. Every per-share number in the bull case quietly assumes those new shares don’t pile up too fast.

A couple more. The insiders have been selling into this run, including the CEO offloading around $10 million worth and a director selling a block. Some of that is scheduled and perfectly normal, but into a vertical move it’s worth clocking. And the laser advantage cuts both ways. That 350% expansion of the laser fabs, plus a shift from four-inch to six-inch wafers, is exactly the kind of manufacturing transition where yield problems hide, and a laser yield problem is a revenue problem.

Finally, two longer-term clouds. There’s a quiet competitive threat from copper and from co-packaged optics. Active electrical cables can now handle the very shortest links (a point Credo hammered on its recent earnings call), and as those and CPO take hold, they can chip away at how many of these pluggable optical modules a cluster even needs. And the whole thing rides on the cyclicality question from the last section. If hyperscaler spending takes a breather, or the inventory whipsaw hits in late 2026 the way LightCounting expects, a richly valued, high-beta, concentrated name is precisely the kind that takes the 50% to 70% drawdown.

The remainder of this article is for premium subscribers. In it, we discuss a valuation for AAOI and the things to watch for investors.