The Race Is Guaranteed. The Winner Isn't - A Breakdown of Aurora

Aurora has the only driverless trucks on the highway. That's not the same as winning.

This week we’re breaking down an autonomous trucking company, Aurora. The central question here is not whether autonomous trucking happens because it does. The question that we need to answer is: who wins and are the winner’s economics as good as everyone hopes?

The reason we’re looking at autonomous trucking is because the total addressable market is absolutely massive. We know that the TAM has to occur because nobody’s just going to sit on their hands and not let this happen. We want to figure out who’s going to win and place our chips on the table.

And in looking at autonomous trucking, we will end up covering other companies in this space over the coming weeks. Companies like Kodiak and maybe taking a look at some private competitors in the space too.

Now for me this is a very interesting topic as well. I drive a Tesla Model Y and I say “drive” but realistically it drives me. The car uses a completely different approach to what Aurora is proposing for trucks and it gets the job done for me. So part of this article will be looking at what Aurora does differently from a company like Tesla and seeing if that is an edge in the long term.

What is Aurora?

In the fewest possible words, Aurora is a company that is trying to solve autonomous trucking.

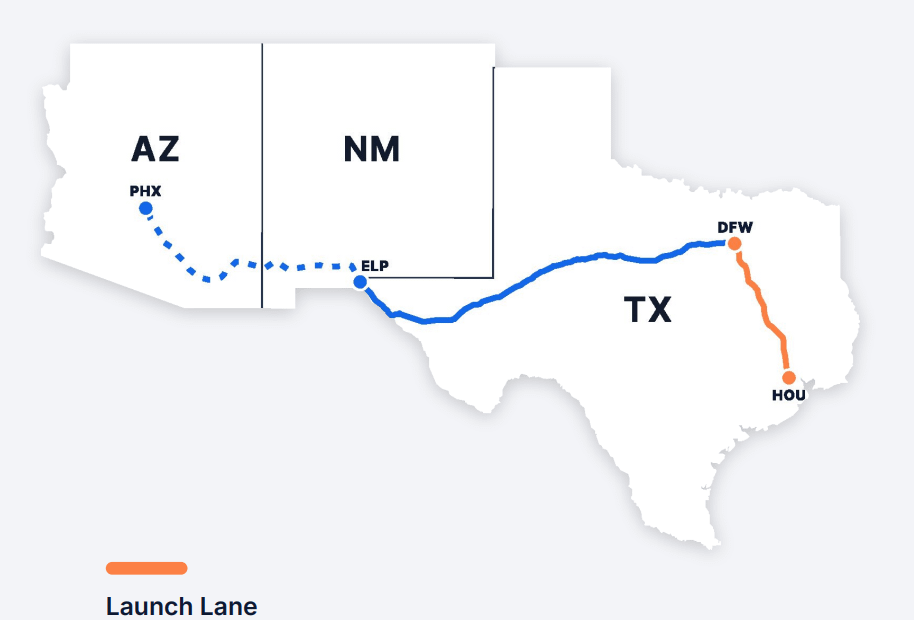

The company today is in the midst of a capital-heavy pilot where it runs autonomous trucks between Dallas and Houston up the I-45 corridor. This is an insanely straight road, very little going on. It’s a highly common route for a lot of freight.

In addition to that route, Aurora is also running between Fort Worth and El Paso and has a 1,000-mile lane between Fort Worth and Phoenix.

As mentioned this is a capital-heavy pilot today where Aurora is building these trucks and then leasing them out as though they were drivers for hire. So anybody looking to move freight between Houston and Dallas can contract with Aurora to move that freight.

Long-term though, Aurora does not want to be in a capital-heavy business. They want to transition into a capital-light driver-as-a-service provider.

In this second phase when they are a Driver-as-a-Service provider, Aurora will provide the software and necessary hardware components for fleets owned by the carriers themselves. Aurora would then charge a per-mile subscription fee for the Aurora driver system.

And that right there is essentially the investment case for Aurora. Can this company get from an expensive phase one pilot, where they are responsible for all the hardware, all the trucks, all the fleet management aspects, to a high margin primarily software business before cash runs out or before competitors do it?

To help them get there they do have a lot of good partners. A lot of big names and logos on the slide decks. OEM names like Volvo, PACCAR, International. Nvidia is a partner for Compute. And they also have customers like Hirschbach, Werner, Schneider, FedEx, Uber Freight, Ryder, and McLane.

How the Aurora Driver Actually Works

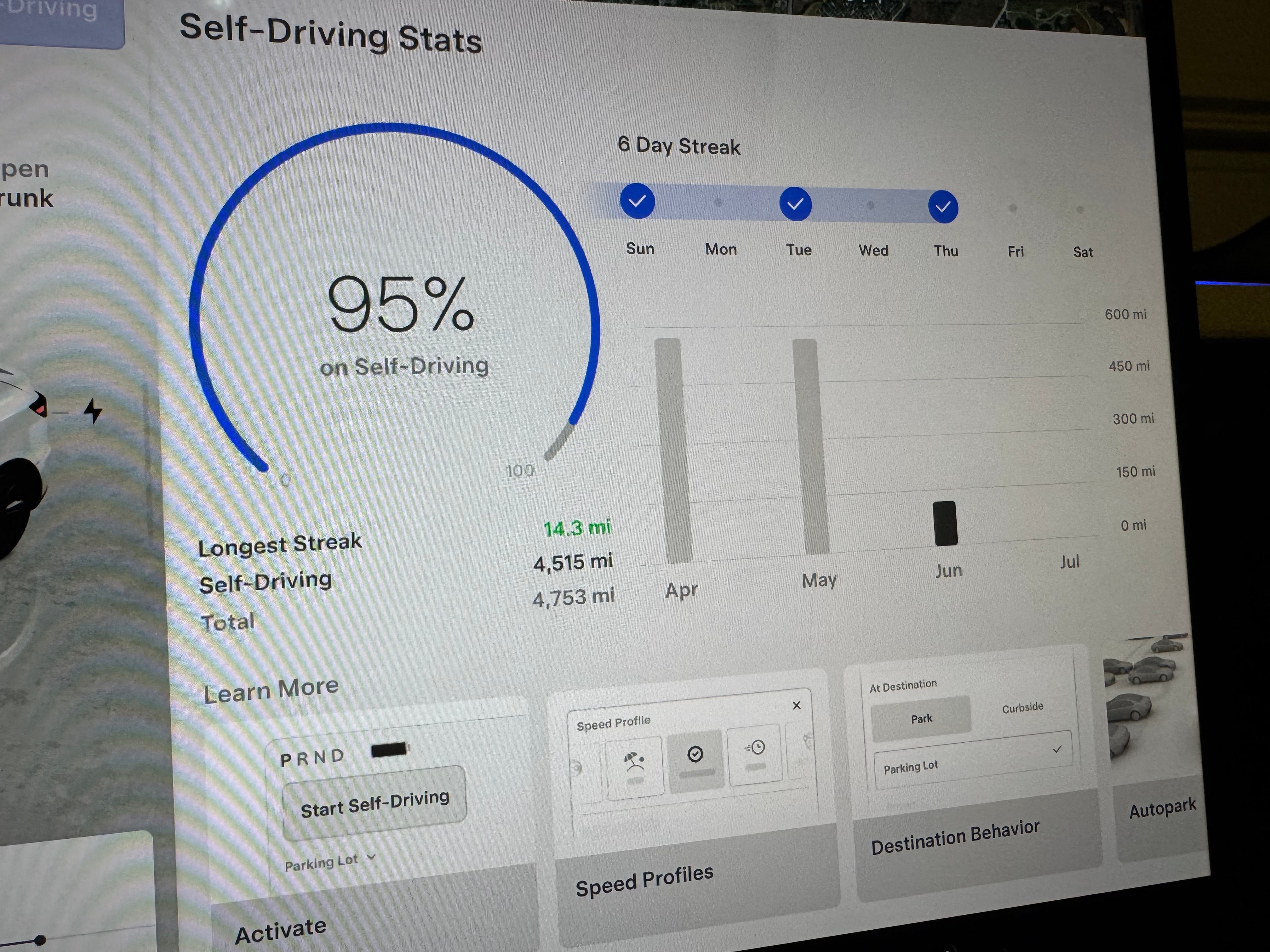

I mentioned in the intro to this piece that I own a Tesla Model Y and I use FSD. Conveniently FSD version 14.3.3 adds this nice new stats screen so I can actually show you how much I don’t drive this car.

As you can see 95% of my miles are not driven by me; they are driven by the vehicle itself and I rarely have to intervene. Most of that 5% is when driving through parking lots or on sections of road where I’d prefer to go a little bit quicker than the car would like.

I’m not just saying this to gloat. I am saying this because Tesla has a very different approach to automation versus what Aurora is doing.

Tesla has placed a bet on vision. The car sees the world through cameras alone and a stack of neural networks turns what they see into driving decisions. There is no LiDAR and that’s on purpose. Elon Musk has previously called LiDAR a crutch. The logic behind that is simple: humans drive with two eyes and a brain so a good enough camera and a good enough brain should be able to do the same. And then you train that system on billions of miles of fleet video and let it learn to drive the way people do. When it works for me and it mostly does, it feels less like a robot following rules and more like a competent driver who happens to live in my dashboard.

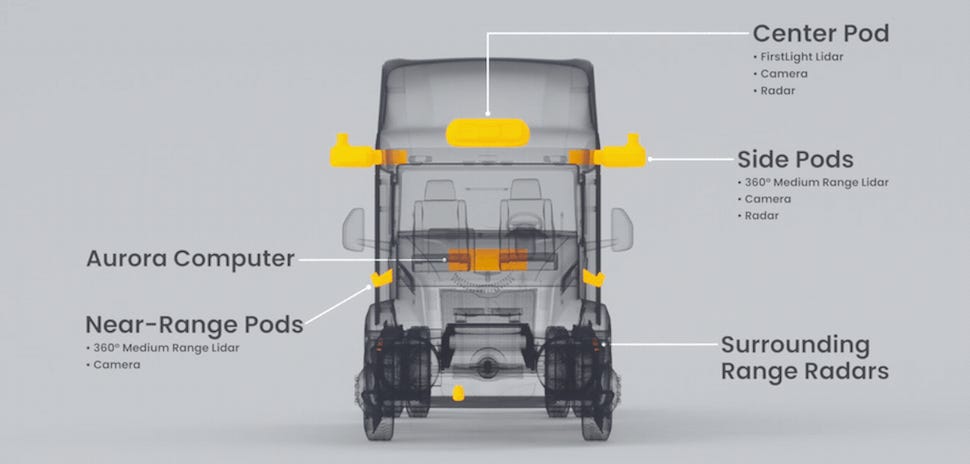

Aurora has gone the opposite way. The Aurora driver does not lean on cameras alone; it carries more than two dozen sensors. Cameras, yes, but also radar and lidar, all working at once, each one covering the blind spots of the others.

The part of the Aurora stack that the company is proudest of is its LIDAR called FirstLight. Most LIDAR fires a laser and times how long the light takes to bounce back, which tells you how far away something is. FirstLight uses a different method called FMCW and it adds one trick that matters a lot. In the same instant that it measures distance, it can also measure how fast every point is moving. A camera has to watch an object across several frames to estimate its speed, but FirstLight just knows. It also sees a long way, with the generation currently being released designed to see around 1,000 meters. Bonus: it works in the dark.

Aurora is not the only company chasing this. Aeva uses the same FMCW approach and, like FirstLight, measures speed directly rather than just distance, though it is aimed more at passenger vehicles and tops out around 500 meters. Hesai is pushing hard on range too, but with conventional time-of-flight lidar rather than FMCW. The point is that the long-range, velocity-sensing approach is real and contested, but nobody else is yet promising the 1,000 meters Aurora is.

That is just the hardware. On the software side Tesla and Aurora’s philosophies split even harder. Tesla lets one large network learn the whole task end to end while Aurora calls its approach “Verifiable AI.”

Verifiable AI blends machine learning with hard-coded rules of the road built so that the company can test them, check them, and prove them. Something like stopping at a red light is not a behavior Aurora hopes the system has picked up from enough video. It is a rule it must follow.

Chris Urmson, Aurora’s CEO, helped build Google’s self-driving program and he has been very blunt that solving driving with pure end-to-end systems leaves you playing whack-a-mole with edge cases forever.

So why does any of this matter if cameras already work well enough in my car?

Because a truck is not a Model Y, a loaded semi weighs up to 80,000 pounds and needs around 500 ft to stop from highway speed. A car needs less than half of that. Spotting a stalled car a thousand feet away instead of 150 turns a hard problem into an easy slow down. Knowing the car’s speed the instant you see it instead of a beat later buys you distance that you cannot win back. If sun glare or a smear on the road blinds one sensor, you badly want others that can still see.

And that is the case for Aurora’s heavier and more expensive setup. Redundancy and range count for more when the thing driving itself weighs 40 tons and there’s no human around to handle it.

My own car does so much with so little and the LIDAR-and-radar-and-everything approach looks like over-engineering. The sort of thing that you’d build when you don’t fully trust the software. After digging in, I still think both things are true at the same time. Tesla has gone a long way to prove that vision alone can drive a car very well in most conditions. Aurora is chasing a harder target where “very well in most conditions” is not the bar because the failure mode is a driverless 40-ton truck.

I’m not ready to call the extra hardware a permanent edge. Sensors themselves keep getting cheaper and software keeps swallowing problems people swore it never would. But for the exact job at hand, taking the driver out of a heavy truck on a highway today, the case for seeing far, measuring speed directly, and never staking the whole system on a single sensor is a strong one.

A quick truck driving primer

I realize we’re going down this path of talking about trucking but haven’t actually spoken about how trucking works today. I mean it looks pretty simple from the outside, right and I guess in a sense it is pretty simple. Somebody picks up a load and they have an agreed-upon rate to deliver that load somewhere else.

Those agreements are usually priced per mile. If you’re delivering a load 1,000 mi, you might charge $2.25 per mile or $2,250 for that load.

You then, the truck driver, would deliver that load, submit all the necessary paperwork, and collect your $2,250 on a net 30 basis, 30 days later.

After you’ve delivered that load and submitted your paperwork, you are now looking for your next load. There’s a near certainty that that next load is not set exactly where you just dropped a load off. Which means you have to drive something called deadhead miles.

Deadhead miles are miles that you, as a truck driver, are not being paid for. Instead it’s driving from one location to another to pick up your next load, which you are being paid for. Deadhead miles are roughly 16% of all miles driven by a truck driver.

Human drivers also have to deal with the intricacies of being human. Humans are only legally allowed to drive for about 11 hours a day give or take. There are a lot of rules that come into play but you cannot drive as a human for 15 hours. Do you know what can drive for 15 hours? That’s right, an automated truck.

Do you know what’s also not wasting hours on driving deadhead? Again an automated truck.

So when you consider trucking at this very high level, there are a ton of benefits to automated trucks happening, which is why I said earlier in the article this will happen. It’s not a case of if, it’s just a case of when and who.

And so talking about price for just a minute, Aurora’s DaaS target is about $0.85 per mile. The company believes that its truck will be able to drive roughly 250,000 miles per truck per year versus a human that is really maxing out about 125,000 miles. So these things end up being insanely cost-effective (if delivered).

Because this is a hub-to-hub or terminal model that Aurora is building out, there’s likely to be a lot of other efficiencies gained there. I’m sure there will still be the trouble of figuring out last mile and how those intricacies work but just doing over-the-road trucking at a rate of 85 cents per mile will change the economy massively.

The TAM, Guaranteed

The total addressable market, which we’ve alluded to throughout, is without a doubt the most interesting story. It is rare that a market will come to fruition. It is rare that you know the size of a market before it can even exist but in the case of automated trucking we have exceptionally good ideas.

And yes this total addressable market is pretty much guaranteed. The winner though is not and Aurora could absolutely be it but it’s also equally likely that one of the competitors gets there first.

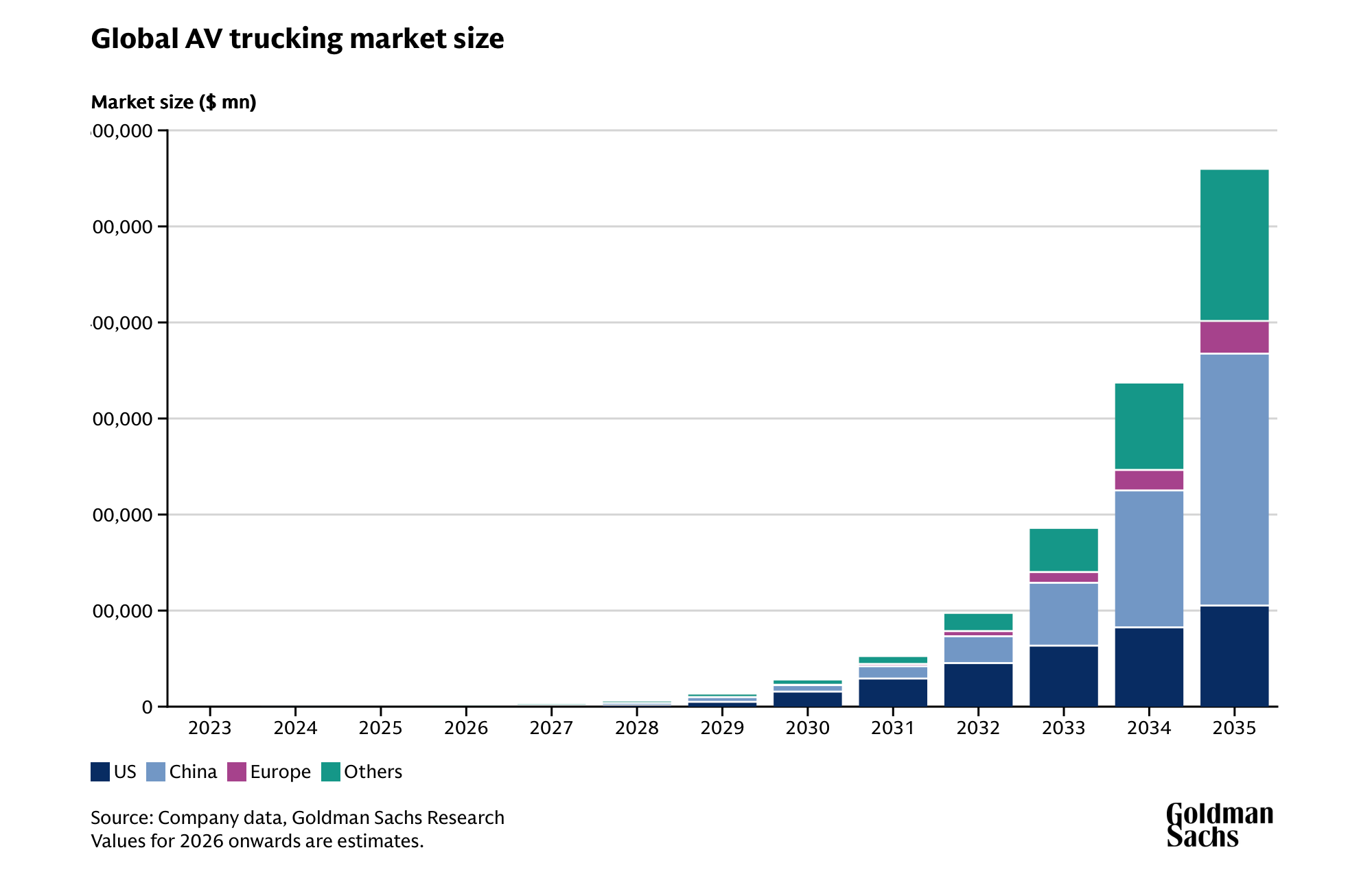

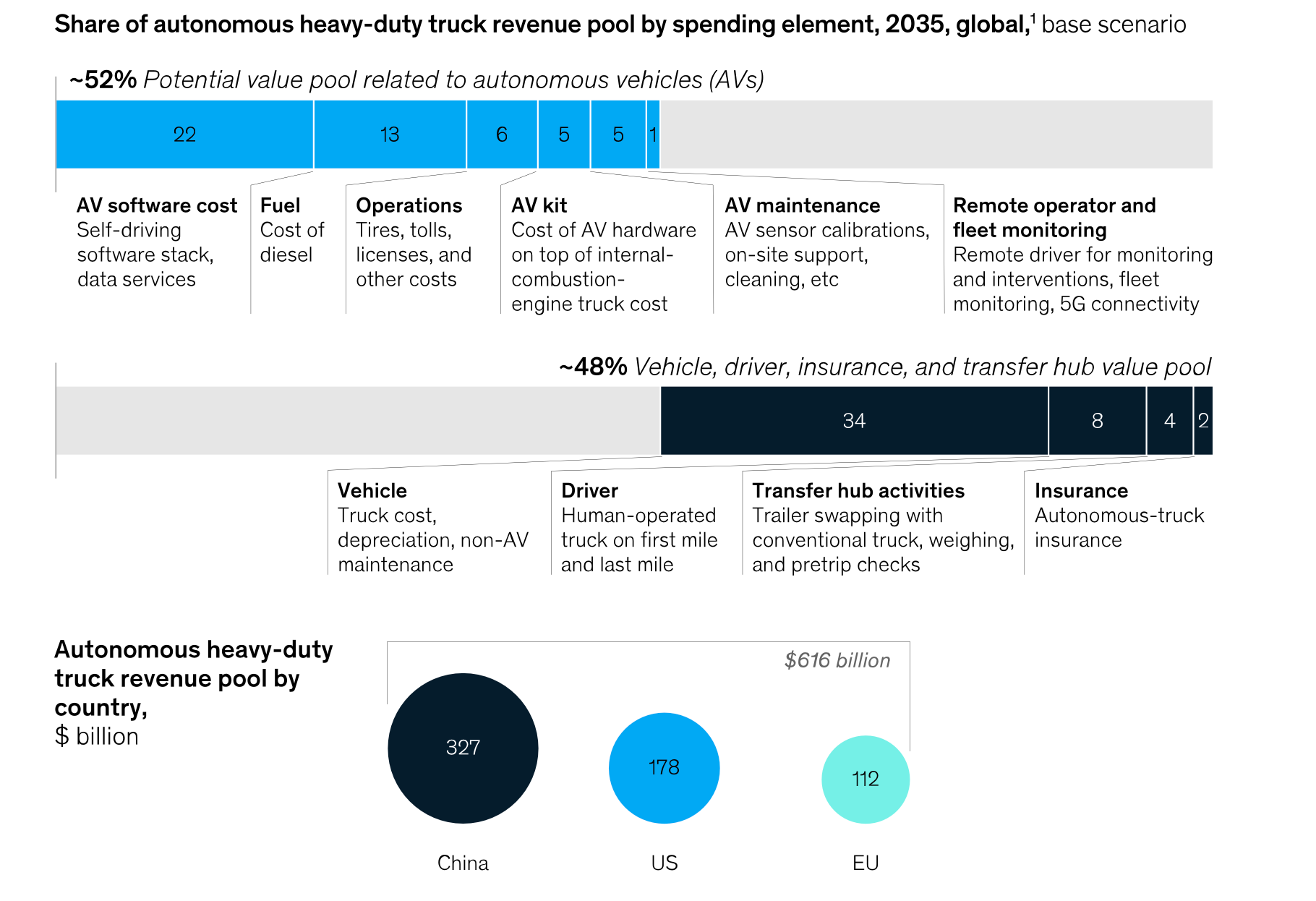

So how big is this total addressable market? Well, Goldman Sachs puts the global autonomous trucking market near $560 billion by 2035 ($105B in the U.S.), which is larger than the robotaxi number that the company has put out there.

They believe that the cost per mile crossover is going to be happening around 2028. That crossover is when it is more cost efficient to hire a robot than it is to hire a human.

Other forecasts include McKinsey, who is more bullish on the US. It forecasts that autonomous heavy-duty trucking could reach $178 billion by 2035. McKinsey’s global figure lands around $600 billion, which is closer to Goldman’s.

Overall US trucking generated $906 billion in gross freight revenues in 2024, just down from about $1 trillion in 2023. It employs 3.58 million professional drivers and 8.4 million people in trucking-related jobs.

Driver wages are estimated to be somewhere around 32-40% of trucking operating costs, which is the single largest cost bucket.

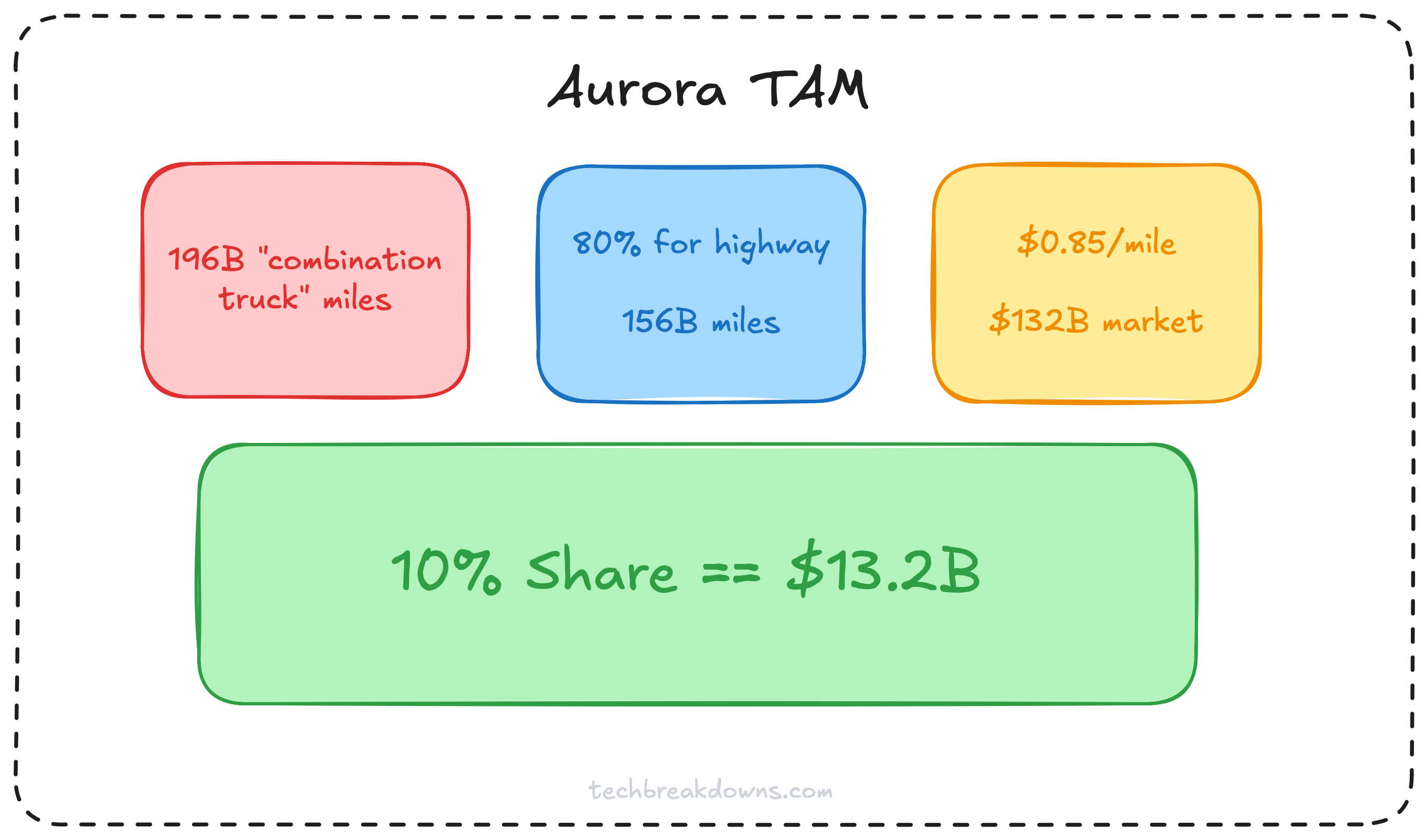

This is a lot of big numbers so let’s bring it back to the one number that really matters: how many miles are being driven each year by truck drivers over the road on highways?

The number I was able to come up with is 196 billion combination truck (where Aurora is targeting) miles in a year. If we roughly guesstimate that 80% of these miles are driven over the road or on highways, that gives us 156 billion miles with which we can build our Aurora model.

156 billion miles at a cost of 85 cents per mile is $132B. Aurora, of course, won’t capture every single highway mile with its DaaS fee but capturing 10% of those highway miles at that 85 cents gives the company potential $13.2 billion in revenue.

Who else is here?

Aurora is not running this race alone. There’s a crowd. The one that matters most is Kodiak, and it’s close enough that it gets its own breakdown next week. There’s a field of private names too, like Waabi and Torc, that I’ll dig into when I cover them. For now just know the competition is real.

What’s more telling is how short that list keeps getting. This is a brutal business. The tech is hard, the timelines are long, and the cash burn is enormous. Companies don’t limp along in this space. They die.

Look at who already tried. UPS, the largest carrier in the country, bet on TuSimple and on Waymo’s trucking arm. TuSimple delisted and moved to China. Waymo shut its trucking program in 2023. Knight-Swift, the largest truckload carrier, bet on Embark. Embark collapsed.

So the two biggest, most sophisticated buyers in trucking placed early bets and both got burned. Neither has committed to anyone since. Picking the winner early has been a great way to lose money. It also means the largest buyers in the country are still on the sidelines, uncommitted, waiting for someone to prove this at scale. That business is up for grabs, and whoever wins it could see their deployments jump overnight.

It might just come down to last man standing.

Product Noodling

This section will likely be a staple going forward in our breakdowns. A chance to talk about what a company could become, about the paths the product could take. Product Noodling.

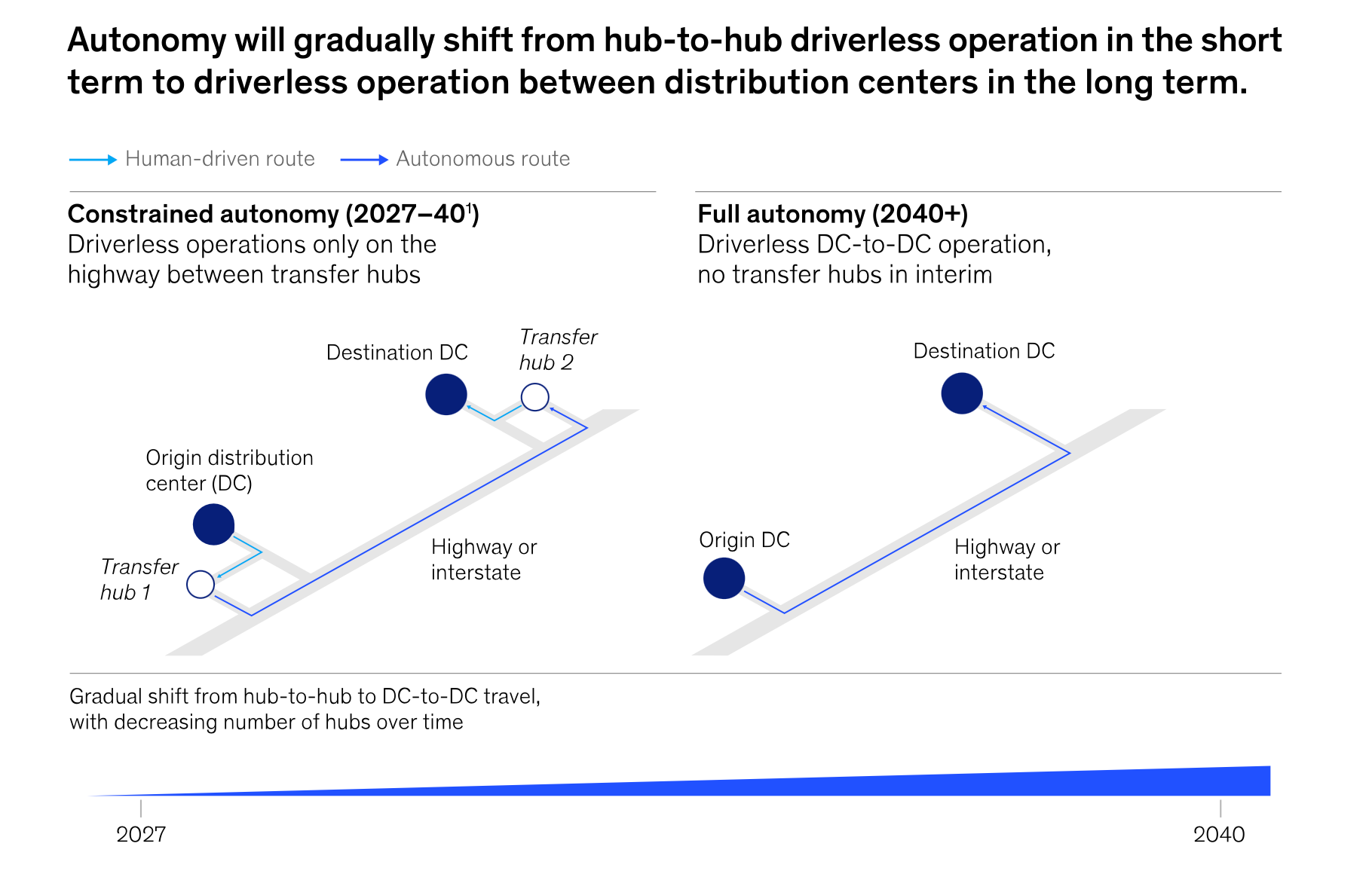

Aurora is a product in its infancy. We know the company wants to go down an asset-light path and build a Driver-as-a-Service offering that carriers of all kinds subscribe to. That’s fantastic. But I want to focus on the part of that dream nobody is really looking at: the logistics.

Today every truck Aurora runs drives over the road only. It runs highway to highway, terminal to terminal. Those terminals are where the over-the-road leg ends and the last-mile leg begins. Until a truck can do the messy last mile by itself, that terminal layer has to exist. The question is who builds it, and who captures the value.

Here’s the tension. Aurora’s asset-light dream has a physical-world dependency. Software trucks still need a national grid of places to stop, and that grid does not exist yet. Someone has to pour the concrete. So Aurora either compromises the asset-light model and builds it, or it stays pure and hands that value, and some leverage, to whoever does.

Because no human is in the truck, these aren’t truck stops. They’re where the truck gets refueled or recharged, where cargo transfers from the long-haul leg to the local one, and where inspections and maintenance happen to keep the thing running. That’s a real operation. There are three ways it can shake out:

Aurora owns it. Most control and the fattest margin per site, but it torches the asset-light story and ties up enormous capital. Given everything Aurora has said, this is the least likely path.

Aurora franchises or licenses it. Aurora sets the standard, certifies the locations, takes a fee, and lets partners put up the capital. This is the real Supercharger parallel, and it keeps the model asset-light while leaving Aurora strategically in the middle.

Somebody else owns it entirely. A Pilot, a Love’s, or a logistics landlord builds the network and Aurora just plugs in. Lowest capital for Aurora, but it captures none of that layer and risks the terminal owner having leverage over it.

Option three does nothing for Aurora. One and two both do, and option two is the interesting one, because it’s the path that fits the business they say they want to be.

So what could licensing actually be worth? Let’s noodle it. Picture a mature network of, say, 150 terminals at the major over-the-road handoff points across the country. If Aurora licenses its standard and takes something like $1 million per terminal per year, in fees, certification, software, and a cut of the services, that’s $150 million a year. Push it to 400 terminals as the network fills in and it’s $400 million. That is real money, and notice what kind of money it is: high-margin, recurring, and asset-light, because the partners funded the buildings. It would sit on top of the per-mile Driver fee, not replace it. None of these numbers are Aurora’s. I made them up to size the prize. But they show the shape of it, a second recurring revenue line that compounds as the truck network grows, without Aurora owning the dirt.

And here’s the part that gives the whole idea teeth: it gets far more powerful if these trucks go electric. A diesel terminal is a service center, useful but not a moat, because a truck can fuel anywhere. An electric terminal is a charging depot, and now you have the actual Supercharger dynamic: proprietary charging, a captive fleet that has to stop where the chargers are, and a location advantage that compounds. So the terminal-as-Supercharger idea is really a bet on electrification as much as autonomy. Today it’s a service network. In an electric future, it’s infrastructure.

I want to be clear that this is speculation, not a forecast. Aurora has not announced any of this, and the asset-light purists would argue they should never touch it. But the terminal layer is coming whether Aurora builds it or not, and a company that already understands these trucks better than anyone, and is already standing up terminals in Texas and Phoenix, is about as well positioned as it gets to be the one that sets the standard.

Below, premium subscribers get access to:

financials review

bull & bear case

valuation

what to watch

what I’m doing in my own portfolio