Monday to Wednesday: What Happens After "Approved"

If you’ve been following along, here’s where we are:

Part 1: The Invisible Handshake covered the chip inside your card, the dead computer that wakes up and runs a cryptographic handshake every time you tap.

Part 2: The 5,000-Mile Sprint followed that proof across Visa’s private network, through a data center in Virginia with a literal moat, to your bank and back. All in under half a second.

Part 3: The Rewards Tax broke down the $100 split: who gets paid, how much, and why the card in your wallet determines the merchant’s margin.

And now, Part 4. This is the final chapter of the payment flow. (We’ll be back for chargebacks and the fraud brain in Parts 5 and 6.)

So far, our story has ended at the moment I walk out of McDonald’s with a Diet Coke in hand. I tapped my card, saw the “approved” message, and went on with my day.

That “approved” was a promise from my bank: “The funds exist and are reserved. We’ll send them.” The bank did not send them. For the merchant, the gap between those two sentences is 1 to 3 business days of working capital sitting in someone else’s hands.

What we’re about to walk through is an “average” store on an “average” timeline. Sometimes things move faster, sometimes slower. But it all starts with a batch close.

The 8pm Cutoff

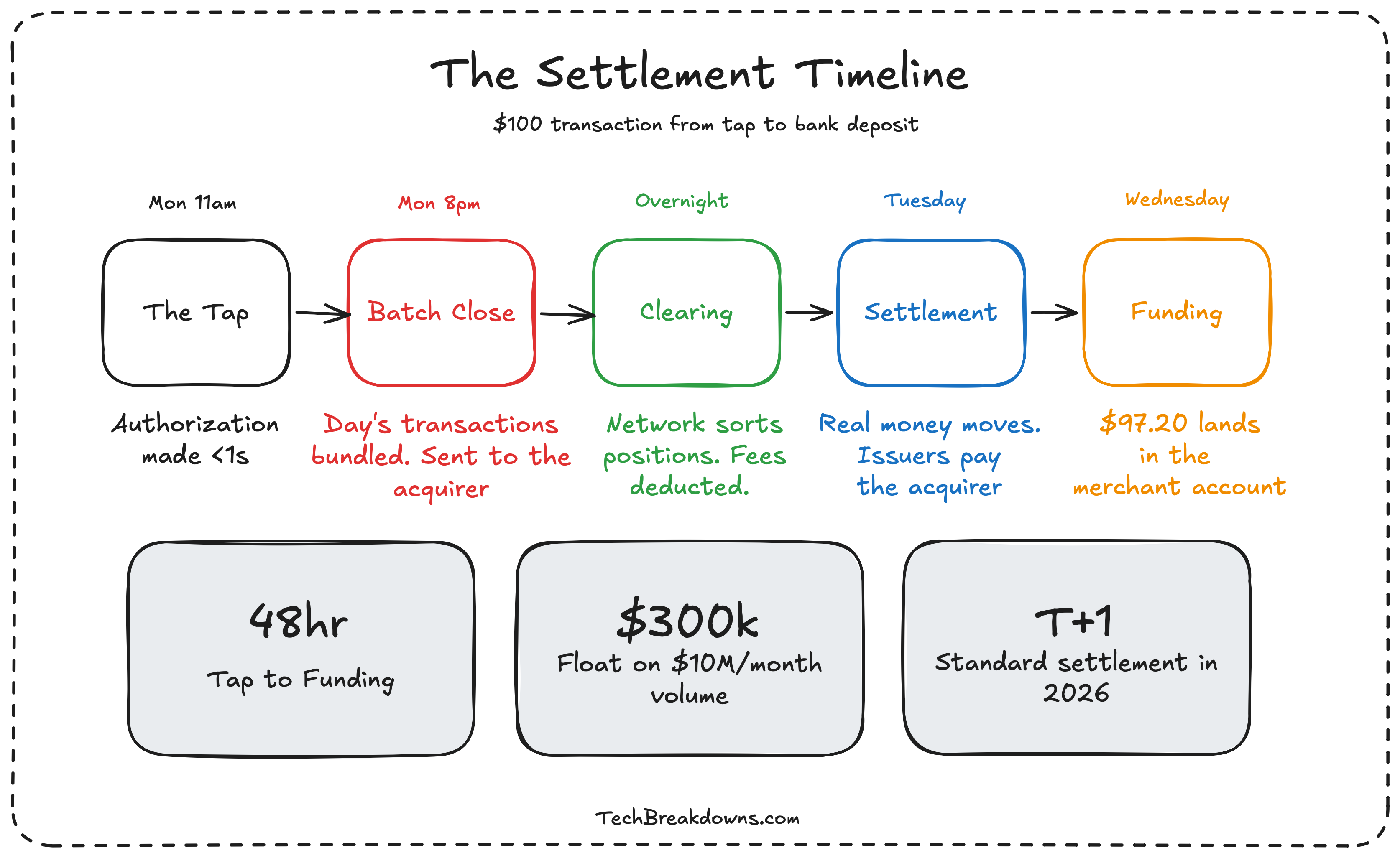

In our story, it’s a Monday. I bought my Diet Coke at 11am. At 8pm, McDonald’s POS system closes the batch.

At a preset time (typically around 9pm, though configurable on most modern processors), the POS system closes the batch automatically. Every authorization code from the day gets bundled into a single file and shipped to the acquirer. My $1.99 Diet Coke, the $47 family meal at register 3, the $8.49 twenty-piece nuggets from the drive-through. Packaged and sent.

The acquirer receives the batch and forwards it to the card network. Visa or Mastercard.

Here the network plays a different role than it did in Part 2. During authorization, the network was a router: move the message, get the answer, send it back. During clearing, the network is an accountant.

It sorts through millions of transactions from thousands of merchants and calculates net positions. How much does each issuer owe each acquirer? The interchange fees from Part 3 get deducted here. The assessment fees too. Every line item, calculated and netted across the entire network.

Still, no money has moved. Just data.

Think of it like airport baggage handling. You walked through the terminal and arrived at your gate in minutes. Your luggage went through a completely separate system: scanned, sorted, loaded, routed. It arrives on its own schedule, through its own infrastructure. And occasionally, it doesn’t arrive at all.

Networks process clearing runs multiple times per day. But the accounting still takes time.

The Money Moves (Finally)

After clearing, the issuers transfer funds to the network. The network distributes those funds to the acquiring banks. The acquiring bank credits the merchant’s account, net of all fees.

On a $100 purchase, the merchant receives about $97.20. That’s the number from Part 3, and this is where it actually lands in a bank account.

But there’s one more step. Settlement (bank-to-bank) and funding (money in the merchant’s operating account) happen separately. Settlement is between institutions. Funding is when the merchant can actually spend it.

For our Monday Diet Coke: batch closed Monday night, clearing ran overnight, settlement completed Tuesday, funding hit McDonald’s account Wednesday morning.

Monday to Wednesday. Three calendar days for a transaction that was “approved” in 400 milliseconds.

And that’s the good scenario. A Friday batch close still typically means funds on Tuesday, sometimes Monday if your processor fronts from their own balance sheet. FedNow operates 24/7 and Fedwire now runs on Sundays, but those are A2A rails. Card settlement still clears through business-day cycles, and the weekend gap hasn’t closed yet for most merchants on standard plans.

The Profitable Delay

So here’s the question: who benefits from the wait?

A restaurant processing $50,000 per month has $1,600 to $3,300 floating in this gap at any given time. A mid-size e-commerce company doing $10 million per month? $300,000 to $600,000 sitting outside their control.

And that’s before reserves. Processors sometimes hold 5% to 20% of monthly volume for 30 to 180 days as collateral against chargebacks and fraud. A new business running $100,000 per month could have $10,000 to $20,000 frozen with the processor. It doesn’t show up in any obvious line item. It just sits there, quietly compounding someone else’s balance sheet.

That someone: the processor. Money in transit between authorization and settlement earns interest. Stripe processed $1.9 trillion in total payment volume last year. Even at T+1 settlement, the daily float on that volume is enormous. Money market returns on billions of dollars in transit add up to a significant, rarely disclosed revenue line.

The push toward instant settlement (T+0) would eliminate this float income (genuinely wild that the incentive structure works against faster payments). Visa Direct and Mastercard Send can deliver funds in near-real-time for gig economy payouts and insurance disbursements. But for standard merchant settlement? Still T+1 at best in 2026.

Stripe Capital exists because of this gap. Square Loans exists because of this gap. The entire merchant cash advance industry, lending businesses money against their own future revenue at effective rates that often exceed credit cards, exists because this float is real, predictable, and exploitable.

The $60,000 Question

Part 3 touched on the processor’s spread. Now let’s do the full math, because every operator hits this wall eventually.

At Stripe’s standard rate (2.9% + $0.30 per online transaction), a company processing $1 million per year pays roughly $29,000 in fees. Actual interchange plus assessment cost: about $23,000. Stripe’s margin: $6,000.

At $1 million, that’s fine. You’re paying for a single API, a unified dashboard, built-in fraud detection, and the fact that your engineers were up and running in an afternoon.

At $10 million per year, the numbers shift. Stripe costs $290,000. Interchange plus assessment: $230,000. Stripe’s margin: $60,000. That’s a full salary.

At $50 million? Stripe’s margin balloons to roughly $300,000 per year. That funds an entire payment engineering team, which is exactly what you’d need to move off Stripe.

The decision framework most operators land on: below $1 million per year, use Stripe or Square and don’t look back. Between $1 million and $5 million, negotiate. Above $5 million, evaluate interchange-plus pricing through Adyen (which processed €1.39 trillion last year at a 53% EBITDA margin) or a traditional acquirer like Fiserv or Worldpay. Above $50 million, you should be looking at a direct acquiring relationship or a payment orchestration layer.

Payment orchestration is the emerging enterprise answer: a software layer that sits above multiple processors, routing each transaction to the cheapest or best-performing option for that specific card type, currency, and geography. The market hit $2.08 billion in 2025 and is projected to reach $18.31 billion by 2035. Stripe launched its own orchestration product in 2025. Adyen has native routing. The signal: the “all-in-one processor” era is giving way to multi-processor strategy at the enterprise level.

The Complete Picture

In Part 1, the chip woke up. In Part 2, the data sprinted across a private network. In Part 3, six different players carved their slice. And now you know the part that actually hits a business’s cash flow: the money takes days to arrive, someone earns interest on the delay, and the platform you chose at $100,000 in annual volume is quietly costing you hundreds of thousands at $10 million if you never renegotiate.

The flow is complete. A $1.99 Diet Coke traveled from a tap on a reader to a batch file at 8pm, through a clearinghouse overnight, into a settlement between banks, and finally into McDonald’s operating account on Wednesday morning.

Four parts. One Diet Coke. A surprisingly long road for $1.99.

Parts 5 and 6 are coming, likely on a bit of a delay as we look at other topics: chargebacks (the dark side of the swipe) and the fraud brain (the AI that decided to approve you in the first place). While we’ve reached the end of the infrastructure story, the business story is just getting started. If you want these future iterations in your inbox, sign up below.