The Rewards Tax: Why Your Free Miles Cost Your Coffee Shop $0.25 Per Latte

Why there’s no such thing as a free flight, and who is actually picking up the tab.

So let’s revisit my Diet Coke addiction.

McDonald’s charges me $1.99 for a large Diet Coke. I tap my standard credit card. They net about $1.94. Five cents, gone. Doesn’t sound like much.

Now picture the person behind me tapping an Amex Platinum. For a merchant paying published rates, that same $1.99 Diet Coke nets closer to $1.84. Same cup. Same ice. Same $1.99. The card in the customer’s wallet determines the merchant’s margin, and the merchant has zero say in it.

(To be fair, this is McDonald’s… they process billions of transactions a year and almost certainly have custom rate agreements that beat the published schedule. More on that in a minute. But the mechanics are the same for every merchant, from a 40,000-location chain to your neighborhood coffee shop.)

Oh, and if you missed the first two parts of this series:

- Part 1: The Invisible Handshake — the chip inside your card

- Part 2: The 5,000-Mile Sprint — where the payment goes after you tap

Now that we know how a transaction flows, let’s talk about what it costs.

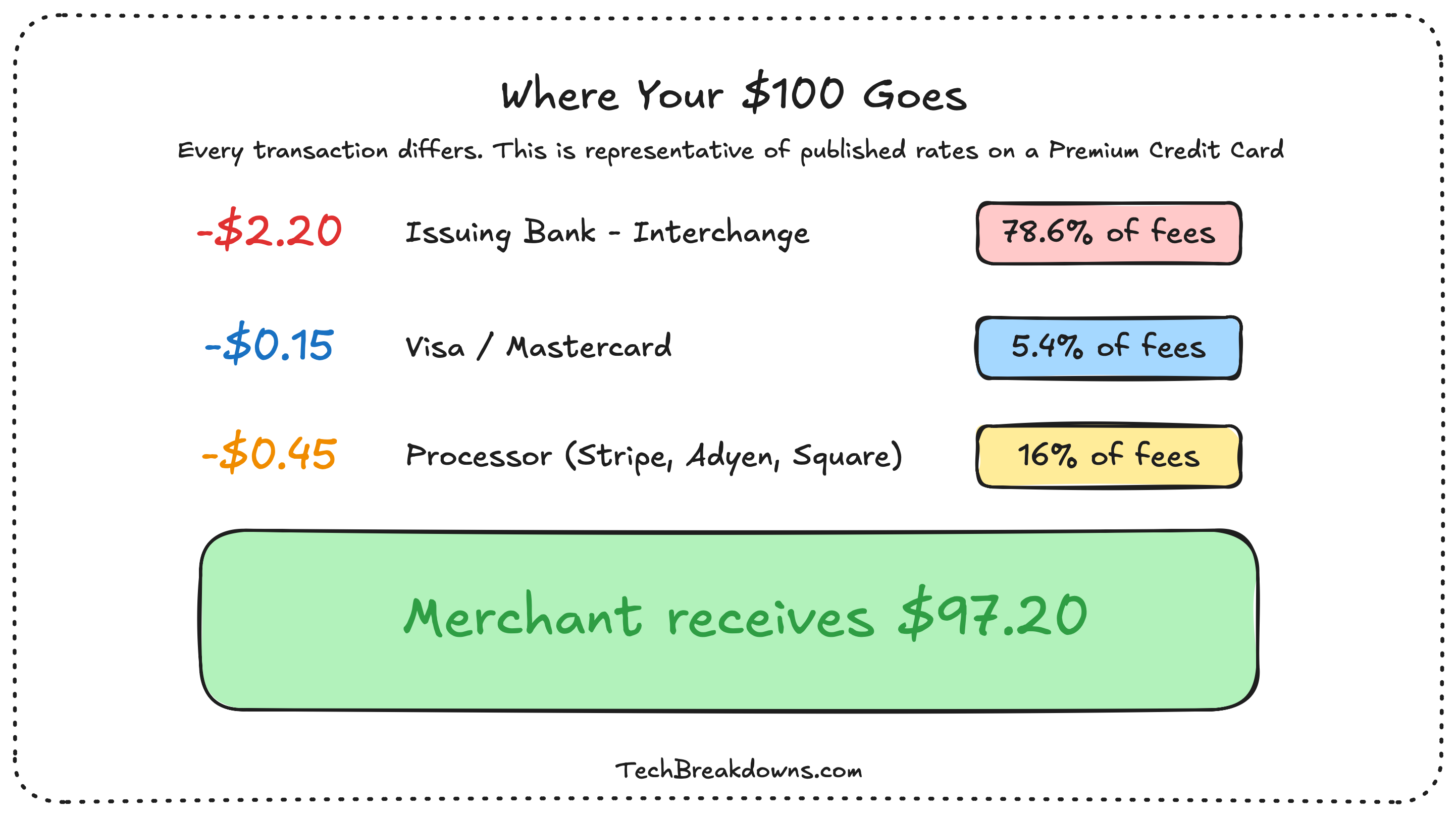

The $100 Split

Because it’s easier to visualize, let’s use a $100 purchase with a premium rewards card. Here’s where your money actually goes:

~$2.20 goes to the issuer (your bank, the one that gave you the card). This is called interchange, and it’s the biggest piece by far.

~$0.15 goes to Visa or Mastercard as an assessment fee. The toll for using those private rails we covered in Part 2.

~$0.45 goes to the processor or acquirer. Names like Stripe, Square, Toast, and Chase Merchant Services live here.

The merchant receives $97.20.

All in, that’s an effective rate of about 2.75% to 3.00% on a typical consumer credit card transaction. For a debit card, you’re looking at 0.5% to 1.0%, thanks to the Durbin Amendment (we’ll get there).

Three cents on the dollar doesn’t sound like a lot. Multiply it by $6.136 trillion in U.S. credit card purchase volume last year, and you start to see the scale of the machine.

The Card in Your Wallet Sets the Price

The fees a merchant pays aren’t flat. Some businesses have better agreements, some have volume deals. But on top of all that, there’s the card type variation. Those premium cards (Amex Platinum, Chase Sapphire) genuinely cost more for a merchant to accept. Here’s the (typical) breakdown:

Basic/Standard

Visa 1.51% + $0.10

Mastercard 1.43% + $0.10

Amex 1.95% + $0.10

Rewards (mid-tier)

Visa 1.65% + $0.10

Mastercard 1.66% + $0.10

Amex 2.40% + $0.10

Premium (Infinite / World Elite / Platinum)

Visa 2.05% + $0.10

Mastercard 1.76% + $0.10

Amex 2.45% + $0.10

Invitation-only / Black cards

3.15% + $0.10

3.15% + $0.10

3.50% + $0.10

That Amex Platinum your friend loves to flash at dinner? It costs the restaurant 2.45% + $0.10 per swipe. A basic Visa debit? About 0.5%. Same meal, same check, wildly different cost to the house.

That $0.10 isn’t a rounding error. It’s a flat per-transaction fee that covers the processing overhead of every authorization, regardless of transaction size. On a $500 appliance it’s noise. On a $6 latte, it’s nearly 2% of the transaction value before the percentage even kicks in. Small-ticket merchants (coffee shops, fast food, food trucks) feel this more than anyone.

Visa and Mastercard rates update twice a year (April and October). Amex sets its own through direct merchant negotiations. These are the published rates, effectively list price. Large merchants with serious volume (think McDonald’s, Walmart, Amazon) negotiate custom interchange agreements that can look meaningfully different. If you’re running 40,000 locations, you have a lawyer in a room with Visa. If you’re running one coffee shop, you’re paying the table.

So Why Does Interchange Exist?

Fair question. And the issuers have a real answer.

Your bank bears the fraud risk. If a fraudulent transaction gets approved, the issuer typically eats the loss. Interchange funds the infrastructure we covered in Parts 1 and 2: the real-time authorization, the cryptographic validation, the fraud scoring, the dispute resolution.

And then there’s the big one: rewards.

Federal Reserve data shows that 86% of interchange revenue flows directly into rewards programs. The six largest U.S. card issuers collectively spent $67.9 billion on rewards last year. Your Chase Sapphire points, your Amex Membership Rewards, your Capital One miles: all funded by interchange.

The economics are perfectly circular. Premium cards generate higher interchange, which funds better rewards, which attract more premium cardholders, which generate more premium transactions. The flywheel spins.

Who’s Actually Paying for Your Flight

And now the math gets uncomfortable.

The person paying cash for a $6 latte gets the same drink as the person pulling out an Amex Platinum. Same price. Same cup. But the Amex customer earns 5x Membership Rewards on dining. The cash customer earns nothing.

The coffee shop paid 2.45% on the Amex transaction and 0% on the cash one. But they can’t charge different prices (network rules historically prevented surcharging, and even where it’s now allowed, most merchants won’t because customers hate it). So the merchant raises prices across the board to absorb the average cost of acceptance. Everyone pays a little more so that rewards cardholders can earn points.

If you’ve ever been to Disney World and bought a Lightning Lane pass, you know this dynamic. You pay extra to skip the line. But the standby queue gets longer for everyone who didn’t pay. The rewards economy works the same way: premium cardholders get the perks, and the cost gets distributed to everyone else, including the people paying cash who get nothing back.

Federal Reserve research documents this transfer directly. The Boston Fed found that each cash-using household effectively pays $149 per year to card-using households, while each card-using household receives $1,133 from cash users annually. The lowest-income households ($20,000 or less) pay $21 per year in this transfer. The highest-income households ($150,000+) receive $750.

The Processor’s Spread

One more player worth knowing: the processor.

Stripe charges 2.9% + $0.30 per transaction, all-in. Stripe pays the interchange to your bank and the assessment fee to Visa, then keeps the spread.

For a small business doing $50,000 a year, that simplicity is worth it. For a business doing $10 million a year, the math changes fast. At 2.9%, that’s $290,000 in processing fees. On interchange-plus pricing (what Adyen offers enterprise clients), the same merchant might pay $220,000. That $70,000 gap is almost entirely Stripe’s margin.

Every business outgrows flat-rate pricing eventually. The question is whether they know it.

20 Years of Fighting (And Counting)

Merchants have been trying to break this system since 2005, when a group of retailers filed an antitrust class action against Visa and Mastercard. The case dragged for 20 years.

In November 2025, a revised settlement was announced: a 0.10% reduction in interchange over 5 years, and a 1.25% cap on standard consumer cards for 8 years.

The catch: 85% of credit cards issued today are rewards cards. The cap applies only to standard consumer cards. The cards generating the highest fees are explicitly exempt (I had to read that twice).

The National Retail Federation called it “all window dressing and no substance.” The settlement is pending court approval, likely in late 2026 or early 2027.

Congress is trying a different approach. The Credit Card Competition Act of 2026, reintroduced by Senators Durbin and Marshall with bipartisan support, would require large issuers to enable routing over at least one non-Visa, non-Mastercard network. If merchants can pick the cheaper network, competition drives fees down. Trump endorsed it on Truth Social, calling swipe fees “an out-of-control ripoff.” As of March 2026, the bill has been introduced in both chambers but hasn’t attached to any legislation yet.

What Happens If Fees Actually Drop

So let’s play it out.

If interchange falls, the $67.9 billion rewards pool shrinks. Your Sapphire Reserve becomes less generous. Your Amex points earn slower. Issuers face a choice: cut rewards, raise annual fees, or find another revenue model.

We actually have a precedent. The original Durbin Amendment capped debit interchange at $0.21 in 2011. Here’s what happened:

Banks eliminated free checking accounts and killed debit rewards programs almost immediately

The Federal Reserve Bank of Richmond found that 98% of merchants either raised prices or kept them the same

Lower-income consumers, who disproportionately used debit, lost free banking products without seeing lower retail prices in return

Merchants saved money. Consumers didn’t.

If the CCCA passes and credit card interchange drops, the same pattern is likely. Merchants keep the savings. Rewards get cut. And the people who built their finances around 2x points and free flights discover those perks were funded by interchange, which was funded by retail prices, which were paid by everyone.

What Happens Next

My $1.99 Diet Coke generated a 5-cent toll. That toll funded a piece of someone’s trip to Cancun, paid for fraud infrastructure spanning four continents, and covered a slice of Stripe’s margin.

The transaction was approved in Part 2. The fees were carved in Part 3. But the money itself hasn’t actually moved yet.

That $1.99 is still floating somewhere between McDonald’s and my bank, waiting for the nightly batch process. The settlement, the actual movement of cash, takes another 24 to 48 hours.

That’s Part 4.